Introduction

Buying committees in enterprise banking now span five to 16 stakeholders across as many as four functions, and 74% of those groups demonstrate unhealthy conflict during the decision process. Sales cycles routinely stretch beyond 12 months. The pressure on enterprise Account Executives heading into 2026 is unlike anything in most other industries.

Banking compounds every challenge. Regulatory scrutiny means vendor decisions can trigger supervisory review. Risk-averse buyers prioritize career safety over bold choices. And payment stablecoin forecasts ranging from $0.5 trillion to $3.7 trillion by 2030 signal that fintech disruption has permanently reshaped the competitive landscape these AEs must navigate.

The bar for enterprise Account Executives (AEs) has never been higher. What follows are the specific skills that separate consistent closers from average performers in banking B2B sales — and what makes this sector require a fundamentally different approach.

TL;DR

- Enterprise AEs in banking need deep domain knowledge: regulatory frameworks, financial metrics, and market fluency

- Risk-averse banking buyers value decision de-risking and air-tight business cases over persuasion tactics

- Multi-threading across CRO, CFO, Compliance, Risk, and Legal is essential — not optional

- AI fluency and data literacy are emerging as baseline requirements heading into 2026

- Scarcest candidates combine strategic selling capability with genuine industry credibility

Why Enterprise B2B Sales in Banking Is Uniquely Challenging

Banking differs from other enterprise sales environments in three critical ways.

Large buying committees with non-commercial veto holders. Harvard Business Review put the average at 6.8 stakeholders in 2017; Gartner now finds groups of 5–16 people across up to four functions. In banking, Compliance, Risk Management, Legal Counsel, and Vendor Management each hold independent veto power—regardless of how enthusiastic the business sponsor is.

Extended procurement cycles driven by regulatory review. The OCC's third-party risk guidance adds formal diligence stages with no equivalent in other industries. Information security reviews, model risk assessments, and regulatory approval processes add 3–6 months to deal timelines before a contract is signed.

Buyer psychology shaped by career-risk aversion. Banking executives operate under constant regulatory scrutiny. A bad vendor choice can trigger enforcement actions, operational failures, or reputational damage—and they know it. Gartner reports 67% of B2B buyers now prefer a rep-free experience. Decision confidence drives closure here, not feature excitement.

The standard B2B playbook breaks down fast in this environment. Great demos, a single champion, and FOMO-based urgency all fail. What works instead is an AE who understands regulatory constraints, can navigate multi-stakeholder committees, and builds the kind of credibility that risk-averse buyers actually trust.

Top Skills for Enterprise Account Executives in Banking B2B Sales 2026

The most effective enterprise AEs in banking combine technical fluency, strategic sophistication, and interpersonal depth. The following five skill clusters define excellence in this space.

Industry & Regulatory Knowledge

Regulatory literacy separates credible sellers from vendor noise in banking. Buyers at banks immediately test whether a seller understands their operating constraints. AEs who demonstrate fluency in key regulatory frameworks earn credibility in minutes that relationship-building alone cannot achieve in months.

Critical frameworks include:

- BSA/AML: FinCEN's Bank Secrecy Act requirements govern anti-money laundering programs, suspicious activity reporting, and customer due diligence

- OCC oversight: The OCC's supervisory expectations for third-party risk management, fintech arrangements, and operational resilience

- FDIC compliance: Deposit insurance requirements, consumer protection rules, and enforcement expectations

- Data privacy obligations: GLBA requirements and state-level privacy laws like CCPA/CPRA

Financial acumen is equally critical. Enterprise AEs must understand how banks measure success: net interest margin (NIM), cost-to-income ratio, return on equity (ROE), and credit loss provisions. Frame your solution's value in metrics that actually drive budget approval. When presenting to a CFO, quantify impact on the efficiency ratio or capital allocation, not just "time savings."

Digital banking transformation awareness elevates AEs from vendor to strategic partner. In 2026, banks face pressure from fintech disruptors, core banking modernization demands, and open banking/API integration trends. Position your solution within this narrative — connecting your offering to imperatives like entering new markets, digitizing customer experience, or cutting operational cost at scale.

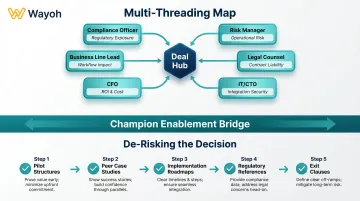

Strategic Stakeholder Management

Multi-threading is a survival skill in banking. The average enterprise deal involves compliance officers, risk managers, legal counsel, IT/CTO, CFO, and business line leadership — all needing engagement. AEs who rely on a single champion consistently lose deals. Effective stakeholder mapping from day one protects momentum.

What does multi-threading look like in practice?

- Identify all stakeholders early through discovery conversations

- Map each stakeholder's priorities, concerns, and veto authority

- Create tailored value narratives for each functional area

- Maintain separate communication threads with business, risk, and technology buyers

- Build redundancy — if your champion leaves or gets sidelined, the deal doesn't collapse

Champion enablement is a distinct skill from simply having an internal advocate. Top AEs actively equip their champion with executive language, business case framing, and risk mitigation arguments needed to carry the deal up the chain.

Create a "champion selling aid": a concise, executive-facing document co-created with your champion that speaks to profitability, risk, and strategic impact rather than features. Your champion shouldn't need to translate your pitch — you should translate it for them.

Gartner research shows tailoring content for "buying group relevance" increases consensus by 20%, while over-optimizing for individual relevance has a 59% negative impact on consensus.

The ability to de-risk decisions addresses the "fear of messing up" (FOMU) dynamic directly. In banking, decision-makers know a bad vendor choice can trigger regulatory scrutiny. Top enterprise AEs get ahead of this through:

- Pilot structures that reduce commitment risk

- Peer case studies from similar-sized institutions

- Implementation roadmaps with clear risk mitigation checkpoints

- References from institutions already under similar regulatory oversight

- Clear exit clauses and support commitments

Make it easier to say yes by making the decision feel safe.

The stakeholder management work above — threading multiple relationships, enabling your champion, de-risking the final call — is ultimately in service of one thing: building a business case the entire buying group can stand behind.

Business Acumen & Value Quantification

Shift from pain-point selling to transformation selling. C-suite banking buyers don't approve large budgets to fix minor inefficiencies. Connect your solution to strategic transformation themes: entering new markets, reducing regulatory exposure, digitizing customer experience, cutting operational cost at scale.

Forrester predicts providers must shift from processing transactions to delivering impactful interactions for large B2B purchases increasingly processed via digital channels.

Build business cases tied to banking KPIs before the demo. Model ROI, cost reduction, risk mitigation value, or compliance efficiency in numbers that a CFO or risk committee can evaluate without speaking to the sales team.

Key considerations from Deloitte's guidance for CFOs include:

- Data quality and interoperability with existing systems

- Integration complexity with the bank's technology core

- Governance and risk management implications

- Vendor strategy tradeoffs and long-term viability

Assume every deal goes to Finance. Build materials accordingly: one-page financial summaries, sensitivity analyses, and payback period calculations.

Project management is a genuine enterprise skill. Long banking sales cycles involve missed tasks, new stakeholders joining mid-deal, competing internal priorities, and complex approval chains. Top enterprise AEs function more like deal project managers than traditional sellers. Use structured timelines, digital deal rooms, and proactive stakeholder updates to protect momentum. Send weekly summaries of progress, next steps, and blockers. Don't wait for the buyer to ask for updates.

Communication & Executive Presence

Translating solutions into executive language is a learned skill. Banking C-suite buyers evaluate vendors through the lens of profitability, risk, regulatory exposure, and market position. AEs who default to feature-level presentations or jargon-heavy decks lose the room quickly.

What does "speaking executive" actually look like?

- Lead with business outcomes, not product capabilities

- Frame solutions in terms of strategic priorities already on their agenda

- Use financial metrics the executive team actually tracks

- Address regulatory implications proactively

- Keep presentations to 3-5 key points, not 15-slide feature tours

Active listening and consultative discovery build trust. In banking relationships, rushing to pitch erodes credibility. Effective AEs spend more time in diagnosis, surfacing the real business problem and its financial cost before presenting any solution. Modern SPIN-style discovery applies perfectly: dive deep into problems and implications, minimize situation questions the buyer assumes you already researched.

Ask questions like:

- "What happens if you don't solve this in the next 12 months?"

- "How does this issue affect your regulatory examination ratings?"

- "Which executive stakeholders are feeling the most pressure on this?"

- "What's the cost of the workaround you're using today?"

Discovery isn't interrogation — it's collaborative problem definition.

2026-Ready Skills: AI and Adaptive Learning

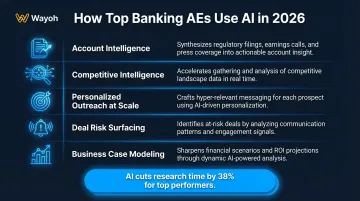

AI fluency is now a baseline expectation for top-performing enterprise AEs. Salesforce reports 90% of sales organizations use some form of AI, with top performers 1.7x more likely to use AI agents — which Salesforce estimates cut research and content-creation time by 38%.

How are top banking AEs using AI?

- Synthesizing regulatory filings, earnings calls, and press coverage to build genuine account intelligence before stakeholder conversations

- Accelerating account research and competitive intelligence gathering

- Personalizing outreach at scale without sacrificing quality

- Surfacing deal risks by analyzing communication patterns and stakeholder engagement

- Sharpening business case modeling through scenario analysis

Meanwhile, 45% of B2B buyers now use AI in purchase decisions. Your buyers are AI-enabled. You should be too.

A fast-learning, low-ego mindset separates good from great. Banking is evolving rapidly: open banking, embedded finance, AI risk management, evolving regulatory frameworks. Enterprise AEs who can rapidly develop credibility in new sub-sectors or product areas without relying on deep prior experience are increasingly valuable.

Korn Ferry identifies learning agility as critical for leadership in uncertain, fast-changing environments, emphasizing agility as a stronger predictor of future success than past experience. In banking specifically, this means being able to:

- Quickly understand new regulatory guidance and its commercial implications

- Adapt messaging when selling to different institution types (community banks vs. digital banks)

- Learn new financial products and their risk profiles

- Pivot strategy when buyer priorities shift mid-deal

How to Identify These Skills When Hiring an Enterprise AE for Your Bank

The most common hiring mistake banking companies make is over-weighting rolodex and industry pedigree while under-weighting strategic selling capability, business acumen, and regulatory literacy. A candidate with 10 years at a top bank may have strong relationships but lack the consultative, multi-threaded, transformation-oriented selling skills required for complex enterprise deals.

The rarest—and most valuable—profile combines genuine banking domain credibility with the strategic skills described in this article.

This profile is typically passive. Top enterprise AEs aren't actively job hunting. They're well-compensated in current roles and unlikely to surface through job boards or keyword-matched resume searches.

This is where specialist recruiting firms with deep banking networks and real candidate relationships provide a distinct advantage. Wayoh, for example, has spent 10+ years placing commercial professionals across community banks, commercial banks, digital banks, and regional financial institutions, operating on a network-first approach that reaches passive candidates before positions are ever posted publicly.

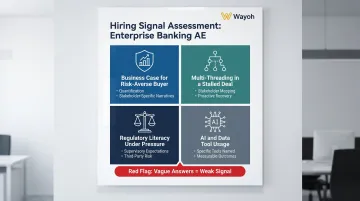

Practical interview and assessment signals:

Business case for a risk-averse buyer. Ask candidates to walk through how they've built and presented a business case for a banking buyer concerned about regulatory risk. Listen for quantification, risk mitigation strategies, and stakeholder-specific value narratives.

Multi-threading in a stalled deal. Ask: "Tell me about a deal that stalled because your champion lost influence or left. How did you recover?" Strong candidates will describe stakeholder mapping, relationship diversification, and proactive risk management.

Regulatory literacy under pressure. Present a scenario: "You're selling into a community bank that just received heightened regulatory scrutiny. How does that change your approach?" Look for references to supervisory expectations, third-party risk management processes, and early Compliance and Risk engagement.

AI and data tool usage. Ask how they've used AI or data tools in their most recent pipeline management. Top candidates will name specific tools and describe concrete use cases with measurable time savings. Vague references to "staying current" are a red flag.

Conclusion

In banking B2B enterprise sales, the skills that separate top performers aren't charm or hustle. They're domain credibility, strategic deal orchestration, and the ability to make complex purchase decisions feel safe for risk-averse institutions. The AEs who master these in 2026 will consistently outperform peers in every market condition.

That applies whether you're an AE sharpening your own skillset or a bank building a commercial team for 2026 growth. Either way, knowing exactly what to look for is where it starts.

If your organization needs help identifying and securing enterprise sales talent that fits this profile, Wayoh's banking specialist recruiters can connect you with candidates from a decade-deep network in the sector. Reach out at hiring@wayoh.co to start the conversation.

Frequently Asked Questions

What is an enterprise account executive salary?

Enterprise Account Executive compensation typically includes a base salary plus variable commission, with total on-target earnings (OTE) structured around a 50/50 split. The Bureau of Labor Statistics reports a median annual wage of $100,070 for technical and scientific sales representatives (May 2024), while Glassdoor data shows SaaS Account Executive median total pay of $197,155. In banking-sector B2B roles, compensation tends to skew higher due to deal complexity, longer sales cycles, and regulatory requirements.

What skills are needed for B2B sales?

Foundational B2B skills include communication, active listening, resilience, and problem-solving. At the enterprise level in banking, these basics must be paired with more advanced capabilities: regulatory knowledge, financial acumen, multi-threading, business case quantification, executive presence, and AI fluency.

What's the future of B2B sales trends for 2025 and beyond?

Key trends include AI-augmented selling (90% of sales organizations now use AI), committee-based buying (teams now span 5-16 stakeholders), the shift from feature selling to transformation selling, and growing importance of regulatory and domain literacy in regulated industries like banking. Buyers increasingly prefer rep-free experiences, demanding that sellers add genuine value through insight and strategic guidance.

What are the 5 C's of sales?

The 5 C's commonly include Competence, Confidence, Consistency, Communication, and Commitment—though definitions vary by framework. In an enterprise banking sales context, each maps to a specific skill demand:

- Competence: Domain expertise in banking regulations and financial products

- Confidence: Executive presence when engaging C-suite buyers

- Consistency: Disciplined follow-through across 9-18 month sales cycles

- Communication: Translating complex solutions into business-language executives understand

- Commitment: Proactive deal management when stakeholder momentum stalls

How long is a typical enterprise sales cycle in banking?

Enterprise B2B sales cycles in banking typically run 9-18 months for complex deals. Regulatory review, third-party risk management, and multi-department approvals extend timelines well beyond other sectors. OCC guidance on bank-fintech arrangements adds formal diligence—security reviews, model risk assessments, compliance sign-offs—that alone can consume 3-6 months.

What makes selling to banks different from other enterprise B2B sales?

Three core differences define banking sales: a uniquely risk-averse buyer culture driven by regulatory accountability, a buying committee that includes non-commercial veto holders (Compliance, Risk, Legal), and a procurement process shaped by regulatory timelines rather than business urgency alone. Gartner research shows 67% of B2B buyers prefer rep-free experiences, and in banking specifically, decision confidence and risk mitigation matter more than product features or relationship strength.