Introduction: Why Regulatory Risk Is Now a Strategic Priority for Banking Teams

The payments industry has never faced more regulatory scrutiny. New entrants, faster payment rails, cryptocurrencies, Banking-as-a-Service (BaaS) arrangements, and open banking have dramatically expanded the regulatory perimeter banks must defend. For banking teams today, regulatory risk sits at the boardroom level — one gap can determine whether your institution can operate, grow, or keep its charter.

The cost of getting it wrong is severe. In June 2024, the Federal Reserve issued a cease-and-desist order against Evolve Bank & Trust for AML program deficiencies, risk management failures, and consumer compliance gaps tied to its fintech partnerships. The bank was barred from onboarding new fintech partners without prior Fed approval, effectively shutting down a core growth strategy.

That case wasn't isolated. An analysis of 124 enforcement actions between January 2023 and July 2024 found that 64% of actions against BaaS sponsor banks focused on AML/BSA shortfalls, with 79% requiring independent lookback reviews.

This guide covers what regulatory risk means in payments, which agencies matter, the key risk categories banking teams face, how to build an effective framework, and critically, what talent you need to manage it.

TLDR

- Regulatory risk in payments spans BSA/AML, consumer protection, data security, third-party oversight, and emerging products like crypto and BNPL

- Multiple federal agencies have overlapping authority: OCC, CFPB, FinCEN, FTC, Federal Reserve, and FDIC

- A strong framework requires written policies, continuous monitoring, and qualified compliance professionalsStrong compliance programs depend on written policies, continuous monitoring, and regular internal testing

- Banks that treat compliance as a growth enabler outperform those viewing it as a cost center

- Payments-specific compliance talent is scarce — finding the right people matters as much as the right technology

What Is Regulatory Risk in the Payments Industry?

Regulatory risk in payments is the risk that a bank or payments company fails to comply with applicable laws, regulations, and supervisory expectations — resulting in enforcement action, financial penalties, operational restrictions, or reputational harm.

The OCC Comptroller's Handbook defines it as "the risk to a bank's current or projected financial condition and resilience arising from violations of laws or regulations or from nonconformance with prescribed practices, internal bank policies and procedures, or ethical standards."

That definition sits adjacent to — but distinct from — fraud risk (which focuses on criminal activity against the institution) and operational risk (which addresses process failures). In payments, all three frequently intersect in the same transaction or product line.

Why Payments Carries Especially High Exposure

Payments sits at the intersection of consumer protection, financial crime prevention, data privacy, and systemic stability. This means multiple regulatory regimes apply simultaneously to the same transaction or product:

- A single ACH debit involves BSA/AML obligations (FinCEN), consumer protection rules (CFPB), data security requirements (GLBA/FTC), and payment network oversight (Federal Reserve)

- Payment processors must comply with federal consumer protection laws, PCI DSS security standards, state money transmitter licenses, and contractual obligations to sponsor banks

- Banks sponsoring payments programs face "know your customer's customer" (KYCC) expectations, meaning they're accountable not just for direct customers but for end-user activity facilitated through those relationships

Regulation by Enforcement

The CFPB and FTC have used enforcement actions to set de facto industry standards — often outpacing formal rulemaking. The CFPB's June 2023 action against ACI Worldwide — resulting in a $25 million penalty for improperly initiating $2.3 billion in unauthorized mortgage payment transactions — sent a clear message: payment processors bear direct regulatory liability for EFTA/Reg E violations, independent of the merchants they serve.

The BaaS Risk Multiplier

Bank-FinTech partnerships and Banking-as-a-Service arrangements create unique regulatory exposure. When a bank extends its charter to third-party activity, the bank remains fully responsible for compliance. The June 2023 Interagency Guidance on Third-Party Relationships makes this explicit:

"The use of third parties does not diminish or remove banking organizations' responsibilities to ensure that activities are performed in a safe and sound manner and in compliance with applicable laws."

Customer-facing activity may distribute across dozens of third parties, but regulatory liability concentrates at the bank charter holder. For banking teams, that means compliance infrastructure — and the people running it — must scale alongside every new partnership, not after problems surface.

The Regulatory Landscape: Key Agencies and Their Mandates in Payments

Payments companies don't answer to one regulator — they typically face simultaneous oversight from several, each with distinct authority and priorities:

| Agency | Payments Authority | Key Focus Areas |

|---|---|---|

| OCC | Charters and supervises national banks | Safety/soundness, BSA/AML, consumer compliance, third-party risk |

| Federal Reserve | Supervises state member banks; operates FedNow and Fedwire | Payment systems oversight, EFTA/Reg E, bank holding companies |

| FDIC | Insures deposits; supervises state nonmember banks | Consumer compliance, third-party risk, BSA/AML |

| CFPB | Enforces consumer financial protection laws | EFTA/Reg E, UDAAP, remittance transfers, open banking |

| FinCEN | Administers BSA | AML/CFT, MSB registration, SAR filing, KYC/CDD requirements |

| FTC | Enforces consumer protection for nonbanks | GLBA Safeguards Rule, Section 5 (unfair/deceptive practices) |

FinCEN's Role: BSA Obligations in Payments

FinCEN requires money services businesses to register within 180 days of establishment and maintain effective AML programs under 31 CFR Part 1022. For banks, BSA obligations in payments contexts include:

- KYC/CDD: Customer identification and due diligence for account holders and payment originators

- Transaction monitoring: Surveillance for suspicious patterns in ACH, wire, card processing, and money transmission

- SAR filing: Reporting suspicious activity within 30 days of detection

- KYCC expectations: Regulators now expect banks to understand not just their direct customers but the end users those customers serve

CFPB's Enforcement Reach

The CFPB has demonstrated it will pursue processors and facilitators, not just merchants. Beyond the ACI Worldwide action, the Bureau's guidance on subscription dark patterns (January 2023) directly applies to recurring payment processors and establishes standards for authorization and cancellation flows.

State Money Transmitter Licensing

State regulation adds complexity. CSBS reports that while 28 states have adopted the Money Transmission Modernization Act (covering more than 99% of transmission volume), multistate operators still face a patchwork of licensing, bonding, and reporting requirements. State-licensed money transmitters processed $5.5 trillion in payments in 2023.

Emerging Regulatory Frontiers

Beyond established frameworks, three developments are actively reshaping compliance obligations:

- Open Banking: The CFPB finalized the Section 1033 Personal Financial Data Rights rule in October 2024. Institutions with more than $250 billion in assets face an April 1, 2026 compliance deadline.

- Real-Time Payments: The Federal Reserve's FedNow service can terminate or restrict participant access for non-compliance — creating new compliance exposure for institutions that treat real-time rails as operationally equivalent to ACH.

- Crypto/Digital Assets: The OCC has confirmed banks may provide digital asset custody and payment-related services, but regulatory classification and supervisory expectations continue to evolve across federal and state jurisdictions.

Key Types of Regulatory Risk Banking Teams Face in Payments

BSA/AML and Financial Crime Risk

Banks face strict liability for BSA program failures and increasingly for the activity of their payments customers. The Evolve Bank enforcement and the October 2024 OCC action against Axiom Bank for BSA/AML deficiencies tied to fintech sponsorship demonstrate this risk.

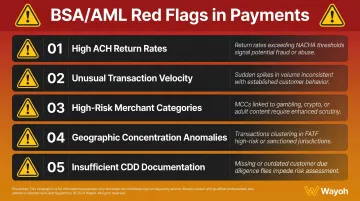

Key risk indicators include:

- High ACH return rates (particularly unauthorized debits)

- Unusual transaction patterns or velocity

- Merchant categories flagged as high-risk (crypto exchanges, online gambling, telemarketing)

- Geographic concentrations inconsistent with stated business models

- Insufficient customer due diligence documentation

Consumer Protection and UDAAP Risk

Unfair, Deceptive, or Abusive Acts or Practices create direct regulatory exposure. The CFPB's UDAAP examination procedures apply to banks and their payment partners.

Common UDAAP violations in payments:

- Misleading billing descriptors that obscure merchant identity

- Unauthorized recurring charges or inadequate cancellation processes

- Failure to honor Reg E dispute rights

- Dark patterns that trap consumers in subscriptions

Banks sponsoring merchants or processors that engage in these practices bear regulatory exposure even when they didn't directly commit the violation.

Data Security and Privacy Risk

Payment systems handle sensitive consumer data, creating multiple compliance obligations:

PCI DSS: Version 4.0.1 became mandatory March 31, 2025, with enhanced requirements for authentication and encryption.

GLBA Safeguards Rule: Applies to banks (supervised by their primary regulator) and nonbank financial institutions (supervised by the FTC). Requires written information security programs, risk assessments, and vendor oversight.

State Privacy Laws: California's CCPA and similar state frameworks create additional compliance layers for payments companies operating across jurisdictions.

Third-party processors and ISOs are often the weak link in a bank's data security perimeter. Regulators hold banks accountable for their vendors' practices.

Third-Party and Vendor Risk

The 2023 Interagency Guidance requires banks to manage third-party relationships across their full lifecycle: planning, due diligence, contract negotiation, ongoing monitoring, and termination.

For payments, this includes:

- Payment processors and ISOs

- Core banking and payment system vendors

- BaaS platforms and middleware providers

- Third-party service providers (TPSPs) handling any payment function

Banks must conduct regulatory due diligence before entering these relationships, maintain continuous monitoring of partner compliance, and ensure contracts include audit rights and regulatory representations.

Emerging Asset and Product Risk

New payment products often outpace existing rules, leaving banks in unsettled regulatory territory:

BNPL: The CFPB issued an interpretive rule in May 2024 classifying BNPL as card issuers under Regulation Z, then indicated it would not reissue the rule due to procedural issues. Regulatory treatment remains unsettled.

Earned Wage Access: Twelve states have enacted EWA laws as of mid-2025, with varying treatment of whether EWA constitutes credit. The CFPB issued a revised advisory opinion on EWA in late 2025; verify current guidance before acting on earlier interpretations.

Crypto: Banks must assess regulatory classification and supervisory expectations for any crypto-related payment activity, which varies by asset type and use case. Stablecoin activity, in particular, faces evolving federal and state-level oversight that differs from treatment of custody or exchange functions.

How to Build a Payments Regulatory Risk Management Framework

Start with a Written Compliance Management System

The OCC Comptroller's Handbook evaluates CMS based on two primary components:

Board and Management Oversight:

- Oversight and commitment (including third-party oversight)

- Change management processes

- Risk identification and management

- Self-identification and corrective action capabilities

Consumer Compliance Program:

- Written policies and procedures

- Consumer compliance training

- Monitoring and audit functions

- Consumer complaint response processes

Regulators evaluate CMS robustness during examinations — and they look at both components together, not in isolation. Your written CMS must document policies, procedures, training requirements, monitoring processes, and escalation paths for all payment products and channels. The framework components below translate these requirements into operational practice.

Core Framework Components

Risk Identification and Assessment

Start by mapping all payment products, channels, and partners to applicable regulations. This includes:

- ACH origination and receipt

- Card processing (acquiring, issuing, or both)

- Wire transfers

- Real-time payment participation

- Digital wallet integrations

- BaaS or embedded finance programs

For each product or channel, identify the applicable federal and state regulations, the agencies with oversight authority, and your specific compliance obligations. That mapping becomes the foundation for everything that follows — including how you monitor.

Ongoing Transaction and Vendor Monitoring

Implement continuous surveillance with clear thresholds and escalation triggers:

- Transaction monitoring rules calibrated to your payment product risk profile

- Vendor performance scorecards tracking compliance metrics

- Consumer complaint trending and root cause analysis

- Regulatory examination findings and remediation tracking

Regulatory Change Management

Establish a formal process for tracking new rules, guidance, and enforcement trends — then build the workflow to update policies when things shift. This includes:

- Subscription to agency alert systems

- Participation in industry associations

- Regular review of enforcement actions for interpretive guidance

- Impact assessments when new regulations are proposed

- Policy update workflows with board and management approval

Board and Senior Management Engagement

The OCC expects boards to "create a culture that prioritizes compliance and holds management accountable" and provide "credible challenge" to management. Boards must receive:

- Compliance risk assessments

- Audit findings and remediation status

- Monitoring reports and alert trends

- Consumer complaint analysis

- Third-party risk management reports

The 2023 Interagency Guidance takes this further — boards must approve and periodically review third-party relationship policies, and receive enough reporting to meaningfully evaluate risk management effectiveness. In practice, this means routine board-level visibility into your payments compliance program, not just annual updates.

Best Practices for Staying Ahead of Regulatory Change in Payments

Implement Continuous Regulatory Monitoring

Subscribe to agency alert systems:

- CFPB updates at consumerfinance.gov

- OCC bulletins at occ.gov/subscribe

- FinCEN news at fincen.gov/news

- FTC GLBA updates at ftc.gov

Track proposed rulemakings: Monitor the Federal Register for advance notices, proposed rules, and final rules affecting payments.

Participate in industry associations:

- NACHA for ACH Operating Rules updates, compliance education, and accreditation programs

- ETA for regulatory advocacy and education specific to electronic payments

- ABA for compliance resources and regulatory guidance for banks

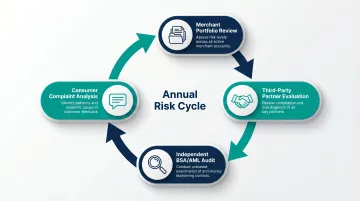

Conduct Regular Risk Assessments and Audits

Perform periodic — at least annual — assessments of your payments risk posture:

- Review merchant portfolios for risk concentration by category, transaction patterns, and return rates

- Evaluate third-party partners against contracted compliance standards and applicable regulatory requirements

- Run independent BSA/AML audits covering transaction monitoring effectiveness, SAR quality, and CDD procedures

- Analyze consumer complaints for systemic patterns before they attract regulatory scrutiny

Feed every identified gap directly into your CMS update cycle with a documented remediation plan — this is what turns assessments into durable compliance improvement.

Build Regulatory Feedback Loops

Establish processes for front-line payments staff to escalate potential compliance issues before they become regulatory problems:

- Log consumer disputes centrally and run trend analysis to catch emerging issues early

- Define clear escalation paths for monitoring alerts — from analysts to compliance officers to legal counsel

- Require formal risk assessment before launching new payment products or partnerships

- Document all supervisory conversations and examination findings with assigned action items and owners

The Talent Dimension: Building the Right Regulatory Risk Team for Payments

Regulatory risk management in payments is as much a human capital challenge as a technology challenge. Automated monitoring tools are only as effective as the compliance professionals who configure, interpret, and act on them.

The OCC Comptroller's Handbook explicitly states that compliance staffing must be "commensurate with the bank's size, complexity, and risk profile" — and that staff must hold "appropriate skills and knowledge of consumer protection-related laws and regulations applicable to the bank."

Key Roles Banking Teams Need

BSA/AML Analysts with Payments-Specific Experience

Not all AML analysts understand payments. Strong candidates bring direct experience with:

- ACH return patterns and typologies

- High-risk merchant category indicators

- Transaction monitoring rule calibration for payment processors

- SAR narratives specific to payments fraud and money laundering

Compliance Officers Who Cover Consumer Protection and Third-Party Risk

Payments compliance extends well beyond BSA. Effective compliance officers need working knowledge of:

- EFTA/Reg E dispute procedures

- UDAAP principles applied to payment products

- Third-party risk management frameworks

- State money transmitter licensing requirements

Legal Counsel Fluent in State and Federal Payments Law

Whether in-house or external, counsel should be able to navigate:

- MTL application and ongoing compliance across jurisdictions

- Federal payment system rules (ACH, Fedwire, RTP/FedNow)

- Enforcement action defense and regulatory response

- Novel product regulatory classification

Risk Officers Who Can Evaluate Emerging Product Lines

As crypto, BaaS, BNPL, and embedded finance continue to evolve, risk officers need to assess regulatory classification and supervisory expectations for products that don't fit traditional categories — often before clear guidance exists.

The Talent Shortage Is Real

Thomson Reuters' 2023 Cost of Compliance Report found that one-third of respondents expected compliance teams to grow while facing increasing difficulty recruiting skilled staff. More than half of firms stated that "shortages of skilled labor will have a high or transformational impact" on their organizations.

The pool of professionals with both regulatory expertise and payments-specific operational experience is limited. Banks competing for this talent face extended search timelines and compensation pressure — and generalist recruiters rarely know the difference between a BSA analyst with ACH experience and one without.

Specialized search firms like Wayoh focus exclusively on compliance, risk, and financial crime hiring across banking and FinTech. With over a decade in the market and 500+ professionals placed, they offer direct access to passive candidates — people not actively job-hunting but open to the right opportunity — who carry the specific regulatory knowledge these roles demand.

Frequently Asked Questions

What is risk management in payments?

Payments risk management is the practice of identifying, assessing, and mitigating financial, operational, legal, and regulatory risks in processing payment transactions. Core risk categories include fraud, chargebacks, BSA/AML compliance, consumer protection, data security, and third-party vendor oversight.

What are the 5 C's of risk management?

In financial risk management, the 5 C's are Character, Capacity, Capital, Conditions, and Collateral. Originating in credit underwriting, these are now applied in regulatory risk contexts to evaluate the risk profile of customers, partners, and payment programs.

What are the key regulatory bodies overseeing the payments industry in the U.S.?

The primary federal agencies are the OCC, CFPB, FinCEN, FTC, Federal Reserve, and FDIC. Each agency targets a distinct risk area — FinCEN owns AML, the CFPB focuses on consumer protection, and the OCC supervises national banks and their fintech partners. State regulators add another layer through money transmitter licensing and privacy laws.

How do banks manage third-party regulatory risk in payments partnerships?

Banks must conduct regulatory due diligence before entering payments partnerships, maintain ongoing monitoring of partner compliance, include contractual representations and audit rights in agreements, and ensure their CMS explicitly addresses how third-party risk is identified and escalated.

What compliance roles should banking teams hire for payments regulatory risk?

Effective payments regulatory risk programs typically require BSA/AML analysts with payments experience, a consumer protection compliance officer, third-party risk specialists, and legal counsel familiar with federal and state payments regulation. Generalist compliance experience rarely translates directly — payments-specific regulatory complexity, from card network rules to FinCEN guidance on money services businesses, demands professionals who have worked inside the industry.