Introduction

Capital markets risk management is the systematic process of identifying, measuring, and controlling potential financial losses from a bank's trading, investment, and lending activities across equity, debt, derivatives, and foreign exchange markets.

For banking teams, this function drives operational discipline — preventing catastrophic losses, maintaining regulatory capital adequacy, and protecting institutional reputation.

Banking risks don't stay in their lanes — they compound quickly. Interest rate volatility can trigger unrealized losses in bond portfolios; those losses can create solvency concerns that spark deposit runs; and inadequate internal controls can turn manageable exposures into billion-dollar failures. The 2012 JPMorgan "London Whale" trading loss — which exceeded $6.2 billion and resulted in $920 million in regulatory fines — demonstrated that even the largest, most sophisticated institutions remain vulnerable when risk management breaks down.

This article covers five types of capital markets risk every banking team must understand: market risk, credit risk, liquidity risk, operational risk, and regulatory/compliance risk. Each arises from different sources, requires different measurement tools, and demands different expertise — and managing them as an integrated system is where most institutions either succeed or fail.

TL;DR

- Capital markets risk management identifies, measures, and controls potential losses from market activity and financial transactions

- Five core types banking teams must manage: market risk, credit risk, liquidity risk, operational risk, and regulatory/compliance risk

- Each type requires distinct tools, governance structures, and specialized expertise

- A single gap — in any one area — can trigger financial loss, regulatory penalties, or lasting reputational damage

- The right risk hires matter as much as the frameworks and technology behind them

What Is Capital Markets Risk Management?

Capital markets risk management is the ongoing process of identifying, assessing, and controlling the potential for financial loss that arises from a bank's activities in equity, debt, derivatives, and foreign exchange markets. This function sits at the intersection of trading operations, investment portfolios, and lending books—covering both the trading side of the institution and its broader balance sheet exposure.

Unlike general corporate risk management, capital markets risk involves faster-moving exposures and more complex financial instruments. A position that looks manageable at market open can become a material threat by market close.

Regulatory frameworks built specifically for financial institutions impose capital buffers, stress testing obligations, and reporting requirements that make this domain distinctly more regulated than non-financial corporate risk. Basel III capital requirements, Dodd-Frank derivatives rules, and MiFID II market conduct standards each add layers of obligation that trading desks and risk teams must navigate daily.

That regulatory structure shapes how banks organize their risk functions. The Office of the Comptroller of the Currency identifies eight core risk categories for bank supervision:

- Credit risk

- Interest rate risk

- Liquidity risk

- Price risk

- Operational risk

- Compliance risk

- Strategic risk

- Reputation risk

Capital markets risk management integrates these categories into a practical, forward-looking framework—guiding banking teams on position sizing, hedging strategies, and capital allocation.

Why Capital Markets Risk Management Matters for Banking Teams

When capital markets risk management fails, the consequences are immediate and severe. The 2012 JPMorgan "London Whale" case remains the most instructive example: a trader in the Chief Investment Office accumulated outsized credit default swap positions that ultimately resulted in a loss exceeding $6.2 billion and regulatory penalties totaling $920 million. The root causes identified by the U.S. Senate Banking Committee included inadequate Value at Risk models, risk limits that were "too broad," poor escalation of concerns, and a unit given "very wide latitude" with minimal supervision. CEO Jamie Dimon testified that management became "complacent" because the CIO had been profitable for years.

Without rigorous risk management, banking teams make decisions without quantified exposure levels, siloed risk functions miss cross-portfolio impacts, and institutions react to market moves rather than anticipate them. Silicon Valley Bank's March 2023 collapse—the largest U.S. bank failure since 2008—illustrated how interest rate risk in a bond portfolio can trigger solvency concerns that spark a deposit run of over $40 billion in a single day.

Both failures point to the same underlying problem: the people managing these risks matter as much as the frameworks themselves. The talent picture is uneven:

- The Bureau of Labor Statistics projects financial analyst employment to grow 6% from 2024 to 2034, with approximately 29,900 annual openings and a 2024 median wage of $101,910

- The OCC's Fall 2024 Semiannual Risk Perspective flags staffing shortfalls in credit risk review and loan workout functions, where "retirements and attrition during the recent benign credit period have decreased the number of experienced professionals"

That OCC-documented gap is where placement decisions become consequential. Wayoh has spent over 10 years placing risk, compliance, and legal professionals across banking teams — 500+ hires — and the pattern is consistent: when experienced credit risk or loan workout talent retires out, institutions often underestimate how long it takes to replace that institutional judgment. Technical regulatory knowledge takes years to build. It isn't easily backfilled.

The 5 Types of Capital Markets Risk Management

Capital markets risk is not a single, uniform exposure. It manifests across five distinct categories, each requiring different monitoring approaches, governance structures, and team expertise. Most banking institutions face all five types simultaneously, and a mature risk function manages them in an integrated way rather than in isolation.

Market Risk

Market risk is the potential for financial loss arising from adverse movements in market prices—including interest rates, equity prices, foreign exchange rates, and commodity prices. This risk affects a bank's trading book, investment portfolio, and balance sheet simultaneously, making it one of the most visible and volatile risk types banking teams manage.

How It Manifests in Banking:

When the Federal Reserve raised interest rates aggressively in 2022–2023, FDIC data shows unrealized securities losses in U.S. bank portfolios surged from $28 billion in Q4 2021 to $470 billion during the rate-rising cycle. Banks holding large bond portfolios experienced immediate compression of net interest margins. A bank structured for stable or declining rates suddenly faced significant unrealized losses when rates spiked.

Foreign exchange swings can erode cross-border portfolio values just as quickly, and equity market downturns directly impact asset valuations and collateral values across the book.

Management Tools:

Banking teams use several quantitative tools to measure and control market risk:

- Value at Risk (VaR) models that estimate the worst expected loss over a given time horizon at a specified confidence level

- Expected Shortfall (ES) calculations that capture tail risk beyond the VaR threshold—now required under the Basel Committee's Fundamental Review of the Trading Book

- Duration analysis to quantify interest rate sensitivity in fixed-income portfolios

- Stress testing scenarios that model extreme but plausible market moves

- Hedging strategies using derivatives such as interest rate swaps, options, and futures

Regulators require documented evidence of these controls. Under the Fundamental Review of the Trading Book (FRTB), banks must calculate capital requirements using both standardized approaches and internal models, with daily fair valuation of all trading book instruments.

Key Limitation:

Quantitative models like VaR can underestimate tail risks during periods of high volatility or low liquidity. The Basel Committee explicitly acknowledged this limitation by replacing VaR with Expected Shortfall as the primary market risk measure. Model outputs must be complemented by scenario analysis and experienced judgment from risk professionals who understand when historical data no longer reflects current market dynamics.

Credit Risk

Credit risk is the potential for financial loss resulting from a counterparty's failure to meet its financial obligations. In capital markets, this includes bond issuers defaulting, trading counterparties failing to settle, derivatives counterparties becoming insolvent, and concentrated sector exposures turning distressed.

How It Appears in Banking:

Credit risk in capital markets moves faster and interacts more directly with market risk than traditional loan portfolio credit risk.

When Archegos Capital Management defaulted in March 2021, Credit Suisse incurred approximately $5.5 billion in losses because the bank failed to adequately manage counterparty credit risk exposure to a family office using total return swaps to build concentrated, leveraged equity positions.

A corporate bond issuer whose credit rating is downgraded mid-transaction can trigger margin calls and collateral requirements. A derivatives counterparty that becomes insolvent leaves the bank exposed to replacement cost risk—the cost to enter a new contract at current market rates. Concentration risk amplifies these exposures: a bank heavily exposed to a single sector that enters distress faces simultaneous credit deterioration across multiple counterparties.

Management Tools:

- Counterparty credit assessments using both internal models and external ratings

- Credit limits and exposure caps that restrict concentration to any single counterparty or sector

- Credit default swaps (CDS) as hedging instruments to transfer credit risk

- Collateral requirements and margining arrangements that reduce exposure

- Credit risk rating models that quantify probability of default and loss given default

Key Challenge:

In capital markets, credit risk escalates rapidly and is often interconnected with market risk. When market prices fall sharply, counterparty credit quality often deteriorates simultaneously, creating compounded exposure that is difficult to model in advance. The Basel Committee's Principles for the Management of Credit Risk mandate that banks must consider "the relationships between credit risk and other risks" and manage credit risk "inherent in the entire portfolio as well as the risk in individual credits."

Liquidity Risk

Liquidity risk in the capital markets context is the risk that a bank cannot buy or sell a security quickly enough to prevent a loss, or cannot meet its short-term financial obligations without incurring significant cost. This risk has two dimensions: market liquidity risk (difficulty exiting positions) and funding liquidity risk (difficulty accessing cash or short-term funding).

How It Surfaces in Banking:

Silicon Valley Bank's March 2023 collapse provides the definitive recent example. The Federal Reserve's review found that SVB, with $212 billion in assets, experienced over $40 billion in deposit outflows on March 9, 2023, and was closed the next day—the largest U.S. bank failure since 2008.

The bank had tripled in size from $71 billion to over $211 billion between 2019 and 2021, funded largely by concentrated, uninsured deposits. When interest rate risk created unrealized bond losses and depositors lost confidence, the institution faced a liquidity crisis it could not survive.

Market liquidity risk appears when a bank holds large positions in thinly traded securities and cannot exit without moving the market against itself. Funding liquidity risk emerges when repo markets tighten, short-term funding sources withdraw, or there is a mismatch between long-term assets and short-term liabilities.

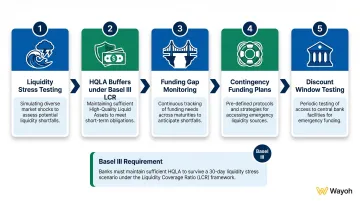

Management Tools:

- Liquidity stress testing that models extreme but plausible withdrawal and funding scenarios

- High-quality liquid asset (HQLA) buffers as required under Basel III's Liquidity Coverage Ratio (LCR)

- Monitoring of funding gaps and maturity mismatches between assets and liabilities

- Contingency funding plans that identify alternative funding sources during stress

- Regular testing of discount window borrowing capacity to ensure operational readiness

Basel III requires banks to maintain "an adequate stock of unencumbered high-quality liquid assets that can be converted easily and immediately in private markets into cash to meet their liquidity needs for a 30 calendar day liquidity stress scenario."

Core Limitation:

Liquidity conditions can deteriorate faster than any model predicts. The September 2019 repo market disruption saw the Secured Overnight Financing Rate (SOFR) spike above 5% in a single day despite banks holding significant reserves, demonstrating how quickly funding markets can seize. Stress tests based on historical data may not capture the speed or severity of a real liquidity event, making real-time monitoring and experienced treasury teams critical.

Operational Risk

Operational risk is the risk of loss resulting from inadequate or failed internal processes, people, systems, or from external events. In capital markets, this spans trade processing errors, technology failures, fraud, data breaches, and human error in high-volume, high-speed environments.

How It Manifests in Banking:

On August 1, 2012, a software error at Knight Capital Group caused the firm to execute millions of unintended trades over a 45-minute period, resulting in losses exceeding $460 million. The SEC found Knight Capital violated market access rules by failing to have adequate safeguards. The loss pushed the firm to the brink of bankruptcy.

Large daily transaction volumes leave little room for error. A single processing failure can create settlement fails, regulatory breaches, and client losses. Operational risk also includes cyber threats, third-party service provider failures, inadequate change management, and the human errors that occur when staff are overworked or undertrained.

Management Approaches:

- Robust systems controls and redundancy to prevent technology failures

- Clear escalation procedures for operational incidents

- Regular internal audits of processes and controls

- Transaction reconciliation protocols to catch errors quickly

- Strong compliance and legal oversight to ensure regulatory adherence

- Investment in technology infrastructure and cybersecurity defenses

The Basel Committee defines operational risk as "the risk of loss resulting from inadequate or failed internal processes, people and systems or from external events." Under finalized Basel III reforms, operational risk capital is calculated using the Standardized Measurement Approach, replacing previous model-based methods.

Key Challenge:

Operational risk is harder to quantify than market or credit risk because many failure modes are rare and unpredictable. The OCC's Fall 2024 Semiannual Risk Perspective identifies elevated operational risk driven by evolving cyber threats, AI-enabled fraud, third-party dependency, and change management failures. That combination—novel threat vectors, legacy infrastructure, and high transaction velocity—means no checklist fully substitutes for judgment embedded across the entire team.

Regulatory and Compliance Risk

Regulatory risk is the potential for financial loss, penalties, or reputational damage arising from a bank's failure to comply with evolving laws, regulations, and supervisory requirements. In capital markets, this includes capital adequacy rules under Basel III/IV, reporting obligations under Dodd-Frank and MiFID II, derivatives clearing requirements, sanctions compliance, and market conduct rules.

Why This Risk Has Grown:

The Basel Committee's output floor phases in through 2027, reaching 72.5% by January 2027. Dodd-Frank Title VII established clearing requirements for swaps and security-based swaps. MiFID II governs trading transparency and investor protection for EU-active banks. Each framework imposes distinct capital, reporting, and operational obligations—and the volume of those obligations has expanded sharply since 2008.

In FY 2023 alone, the CFTC filed 96 enforcement actions resulting in over $4.3 billion in penalties, restitution, and disgorgement. Cumulative recordkeeping penalties on 20 financial institutions since FY 2022 totaled $1.117 billion, with individual fines reaching $75 million per institution. At that enforcement pace, regulatory risk isn't a tail event—it's a recurring operating cost for institutions without mature compliance infrastructure.

Management Tools:

- Dedicated compliance and legal functions that monitor regulatory change

- Regular internal policy updates to reflect new requirements

- Regulatory reporting teams that ensure timely, accurate submissions

- Staff training programs on new regulatory obligations

- Engagement with regulators during rulemaking periods to understand expectations

- Integrated risk and compliance governance that embeds regulatory requirements into decision-making

Key Limitation:

Regulatory environments differ by jurisdiction, and banks operating across multiple markets face the added complexity of navigating non-harmonized rules. A gap in compliance expertise in any one jurisdiction can trigger enforcement action across the broader institution. The OCC's heightened standards for large banks establish minimum risk governance requirements, and a December 2025 proposed rule would increase the asset threshold from $50 billion to $700 billion, expanding regulatory scope.

How Banking Teams Prioritize Capital Markets Risk

Banking teams don't choose one type of risk to manage—they must manage all five simultaneously. The weight given to each depends on the institution's size, business model, and market exposure.

A community bank with limited trading activity will prioritize credit and regulatory risk. A large investment bank with an active trading book dedicates far more resources to market and operational risk management.

Key Prioritization Factors:

- Institutions with large proprietary trading desks carry elevated market and operational risk exposure

- Banks operating across multiple countries face compounded regulatory complexity that smaller domestic institutions don't

- Derivatives portfolios and structured products require more sophisticated measurement tools and specialist oversight

- Past losses or regulatory findings often directly shape where resources and attention flow next

Effective prioritization requires both quantitative inputs (risk metrics, capital at risk, VaR outputs) and qualitative judgment from experienced risk professionals. The quality of the team executing risk management is as important as the framework itself.

That makes talent strategy a risk decision in its own right. Wayoh has spent over a decade placing risk and compliance professionals across banking teams—from Credit Risk Officers and Operational Risk Managers to Compliance Analysts. Building the right specialist bench across these five domains isn't just an HR exercise; it directly determines how well an institution can absorb and respond to risk events.

Common Mistakes Banking Teams Make in Capital Markets Risk Management

Even well-resourced banking teams fall into predictable traps. These four mistakes show up repeatedly — and each carries a documented cost.

Siloed Risk Functions

Market risk and credit risk are often correlated during stress events. When equity markets fall sharply, counterparty credit quality frequently deteriorates at the same time. Siloed teams miss these compounding exposures that an integrated view would catch.

The London Whale case made this concrete: the CIO's trading strategy "was not reviewed outside of the CIO," and risk limits were too broad with no granular controls for the synthetic credit portfolio.

Over-Reliance on Quantitative Models

VaR models, stress tests, and credit scoring tools are useful — but not infallible. The Federal Reserve's Silicon Valley Bank review found that management "changed its own risk-management assumptions to reduce how these risks were measured rather than fully addressing the underlying risks."

JPMorgan's experience reinforces the point. A new VaR model introduced in January 2012 "significantly understated the risk" during the London Whale episode. Models need experienced human judgment alongside them, not in place of it.

Compliance Treated as a Separate Lane

Banks that wall off compliance from risk management create blind spots: regulatory requirements get met on paper but don't shape actual risk decisions. Integrated governance — where risk and compliance share decision-making authority — closes that gap.

Operational Risk as an Afterthought

Operational risk is harder to model and lower-visibility than market or credit risk, so it receives less resource allocation. That calculus typically shifts only after an incident, and by then the cost is real.

The OCC's Fall 2024 report documents staffing shortages in cybersecurity and change management — exactly the functions where operational risk is rising fastest due to digital transformation.

Frequently Asked Questions

What is capital markets risk management?

Capital markets risk management is the process of identifying, measuring, and controlling potential financial losses arising from a bank's activities in equity, debt, derivatives, and foreign exchange markets. It protects earnings, capital, and regulatory standing.

What are the main types of risk in capital markets?

The five core types are market risk, credit risk, liquidity risk, operational risk, and regulatory/compliance risk. Each arises from a different source and requires different management tools, governance structures, and team expertise.

What are the main types of risk management?

The four broad approaches are risk avoidance, risk reduction, risk transfer, and risk retention. Capital markets teams typically combine all four, selecting the appropriate strategy based on the risk type and exposure level.

What are the 5 steps of risk management?

The five steps are: identify the risk, assess its likelihood and impact, develop a mitigation strategy, implement controls, and monitor and review continuously. In banking, this cycle runs across all five risk types without pause.

What are the 4 pillars of risk management?

The four pillars are risk identification, risk assessment, risk mitigation, and risk monitoring. In banking, governance and reporting are often added as a fifth pillar due to regulatory requirements for documented frameworks and board-level oversight.

What are the four types of capital markets?

The four types are equity markets (stocks), debt markets (bonds), derivatives markets (options, futures, swaps), and foreign exchange (forex) markets. Banking teams operate across all four, and each carries a distinct risk profile requiring specialized management.