Introduction

Instant payment systems have fundamentally rewritten the rules of banking. Zelle moved $1.2 trillion in 2025; The Clearing House's RTP network processed $246 billion with 94% year-over-year growth; FedNow surged 645% in transaction volume from Q3 2024 to Q3 2025. These systems settle funds in seconds, not days, and operate 24/7/365, a sharp contrast to the ACH and wire rails that once gave compliance teams hours or days to review suspicious activity.

That speed is also the core compliance problem. Traditional AML frameworks were built for batch processing and manual reviews, not sub-10-second settlement environments where funds become irrecoverable the moment they land. The fraud landscape has shifted accordingly:

- Synthetic identity fraud increased eight-fold in 2025

- Deepfake fraud surged 700% in fintech

- Legacy monitoring systems generate false positive rates "in the high 90s" percent, overwhelming analysts while sophisticated actors move money before detection

This article covers what banks and FinTechs need to do differently: move from reactive batch monitoring to real-time risk scoring, use AI to cut false positive noise, and hire the specialized compliance talent that technology alone cannot replace.

TLDR

- Instant payments kill the time buffer AML controls depend on — pre-transaction scoring is now the baseline

- Batch processing, static KYC, and manual sanctions screening can't keep pace with sub-10-second settlement

- Fraud typologies like APP fraud, mule networks, and synthetic identities are purpose-built for instant rails

- Effective defense requires layered controls: real-time scoring, AI monitoring, and continuous sanctions screening

- BSA officers, AML analysts, and financial crime technologists with real-time experience are the critical differentiator

How Instant Payments Are Reshaping the Financial Crime Landscape

What Instant Payments Are — and How Fast They Settle

In the U.S., instant payments settle in seconds through three primary systems:

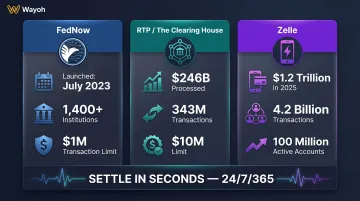

- FedNow — Launched by the Federal Reserve in July 2023, with over 1,400 participating institutions by July 2025 and transaction limits of $1 million

- RTP (The Clearing House) — Processed $246 billion across 343 million transactions in 2024, with limits increased to $10 million as of February 2025

- Zelle — Moved $1.2 trillion in 2025 across 4.2 billion transactions, with 100 million accounts using the platform in December alone

These systems operate 24/7/365 — a sharp contrast with ACH (1-3 business days), Same-Day ACH (hours), and wires (same-day during Fed hours). According to FedNow volume statistics and RTP year-end data, once a payment initiates, funds are settled and gone within seconds.

Volume Growth Outpaces Control Infrastructure

Zelle alone averaged $3.4 billion per day in 2025, with a single-day record exceeding $9 billion in August. RTP averaged over 1 million payments per day by December 2024, with 42% occurring overnight, on weekends, or holidays. The Federal Reserve notes that 66% of surveyed businesses are likely to use instant payments if their primary bank offers them. Zelle growth announcement

That volume doesn't pause for business hours — and neither do the threats embedded within it.

The compliance challenge: Banks must now monitor and screen over 1 million daily payments on RTP alone, with most settlement occurring outside traditional business hours when staffing is thinnest.

Why Speed Favors Bad Actors

In traditional payment systems, delays create intervention opportunities. A suspicious ACH transfer flagged within 24 hours can be reversed before final settlement. A wire might be recalled if caught during Fed hours.

Instant payments remove that buffer entirely. Once funds settle, recovery is nearly impossible. Bad actors exploit this window by executing a rapid sequence:

- Initiating transfers across multiple accounts within minutes of receipt

- Layering funds before any compliance alert is generated

- Withdrawing or converting assets before a human reviewer is even notified

This makes pre-transaction detection and real-time monitoring the only viable defenses. Post-transaction review is useless when the funds are already gone.

Why Traditional AML Controls Break Down at Speed

The Batch-Processing Mismatch

Most legacy AML systems analyze transactions hours or even days after settlement. They run in scheduled batches — often overnight — generating alerts for analysts to review the next business day. By that time, a fraudulent instant payment has long since moved through multiple mule accounts or been withdrawn as cash.

McKinsey reports that many institutions run false positive rates "in the high 90s" percent, while best-in-class players have reduced rates to "the 60s" by using advanced modeling. This means 90-95% of AML alerts are false positives, burying real threats under mountains of noise.

Static KYC Cannot Keep Pace

Traditional Know Your Customer (KYC) and Customer Due Diligence (CDD) processes were designed for periodic, manual reviews — typically at account opening and then annually or when triggered by specific events.

Instant payments demand the opposite: continuous, dynamic risk profiling. A customer whose account shows normal activity one day may suddenly initiate a series of high-velocity transfers the next, indicating account takeover or mule activity. Static KYC snapshots miss this shift entirely.

Sanctions Screening Cannot Fit in 10 Seconds

Ten seconds is not enough time for conventional sanctions screening — verifying each transaction against OFAC and other watchlists sequentially can take just as long as settlement itself.

Banks must shift to customer-level screening continuously refreshed against centralized sanctions databases. That means screening counterparties at onboarding, then re-screening automatically as updated lists publish — decoupling sanctions compliance from the transaction window entirely.

False Positives Create Analyst Fatigue

In a real-time environment, high false positive rates become operationally catastrophic. When 95% of alerts are false, analysts waste hours chasing phantom risks while genuine threats slip through. The result is:

- Delayed response times to actual suspicious activity

- Analyst burnout from reviewing endless low-quality alerts

- Higher compliance costs without commensurate risk reduction

- Regulatory scrutiny when examiners discover missed red flags

Regulatory Expectations Are Evolving

FinCEN proposed a rule in June 2024 (FIN-2024-FCT1) to "strengthen and modernize financial institution AML/CFT programs," explicitly requiring risk-based program design. The rule mandates that compliance resources be directed toward higher-risk activities — a direct challenge to blanket, batch-based monitoring that treats all transactions identically.

Three additional regulatory signals reinforced this direction:

- July 2024: The OCC, FDIC, and Federal Reserve issued a joint interagency statement aligning BSA compliance rules with FinCEN's proposed requirements

- September 2025: FinCEN issued a Request for Information on AML compliance costs, signaling direct regulatory scrutiny of cost-effectiveness

- 2026: The U.S. Treasury's National Money Laundering Risk Assessment warned that rapid fintech growth can "drive volume beyond the capacity of compliance staffing and controls"

Institutions relying on batch processing face growing examination scrutiny as regulators expect demonstrable real-time detection capability.

Common Financial Crime Typologies Targeting Instant Payments

Synthetic Identity Fraud: The Fastest-Growing Threat

Synthetic identity fraud — where fraudsters combine real and fabricated information to create patchwork identities — is reportedly the fastest-growing financial crime facing the U.S. payment system, according to the Federal Reserve.

Key statistics:

- LexisNexis reports that synthetic identity fraud frequency increased eight-fold in 2025, now accounting for 11% of all reported fraud globally

- Equifax estimates annual losses at $20 billion to $40 billion, with 95% of synthetic identities successfully passing initial onboarding

- The Federal Reserve found that traditional fraud models fail to catch 85-95% of synthetic identities, while specialized ML tools can flag 85% of synthetic credit applications

Synthetic identities are particularly dangerous in instant payment environments because they age undetected. Fraudsters open accounts, build transaction history over months, then pivot to high-velocity instant payments before banks can react. Once funds move, recovery is nearly impossible.

Mule Account Networks

Mule account networks use coordinated rings of consumer or small business accounts to receive and rapidly redistribute fraudulent funds in smaller amounts, exploiting the speed of instant rails to disperse money before alerts trigger.

How it works:

- Initial fraudulent funds land in a primary mule account via instant payment

- Within minutes, the account holder (witting or unwitting) initiates multiple smaller instant transfers to secondary mule accounts

- Secondary accounts repeat the process, creating a dispersion chain across jurisdictions

- By the time compliance teams identify the primary mule, funds have moved through 5-10 accounts and are unrecoverable

The UK Finance Annual Fraud Report notes that even in mature instant payment markets, "many banks don't monitor mule risk in real-time."

AI-Enhanced Social Engineering and Phishing

Fraudsters now use large language models and generative AI to produce highly convincing phishing messages, spoofed communications, and fabricated documents that are far more realistic than earlier attempts.

Deloitte reports that deepfake incidents increased 700% in fintech in 2023, while U.S. fraud losses totaled $12.3 billion and are projected to reach $40 billion by 2027.

The FBI's Internet Crime Complaint Center warned in December 2024 that criminals are using AI-generated text specifically "to appear believable to a reader in furtherance of social engineering, spear phishing, and financial fraud" — a direct threat to instant payment authorization workflows.

Common tactics:

- AI-generated deepfake voice calls impersonating bank executives or family members to authorize urgent transfers

- Phishing emails with AI-written text that mimics legitimate bank communication styles

- Fabricated documents (invoices, contracts) generated by AI to support fraudulent payment requests

- Chatbots posing as customer service to harvest credentials

LexisNexis reports that malicious bot attacks increased nearly 60% in 2025, while agentic AI traffic surged 450% — both factors complicating real-time fraud detection.

Authorized Push Payment (APP) Fraud

APP fraud occurs when victims are socially engineered into willingly authorizing transfers to fraudster-controlled accounts. Because the victim initiates the payment, it falls outside traditional fraud detection frameworks that focus on unauthorized access.

U.S. instant payment context:

No U.S. regulator publishes standalone APP fraud figures for domestic instant rails. However, UK Finance data provides a documented comparator: in 2023, 98% of UK APP fraud occurred via Faster Payments (the UK's instant payment system), totaling GBP 380.2 million across 409,533 fraudulent payments. 76% of cases originated from online sources where banks have no visibility until the payment is initiated.

McKinsey found that 77% of customers would leave their bank if it failed to refund a scam loss, while only 6% of financial institutions report an intention to reimburse all scams — a significant customer expectation gap.

Why instant payments amplify APP fraud risk:

- Victims authorize payments under time pressure ("wire the money now or your account will be closed")

- Instant settlement leaves no window for victim realization or bank intervention

- Once funds reach the fraudster's account, recovery is nearly impossible

- Traditional fraud models flag unauthorized access, not authorized-but-coerced payments

Cross-Border Instant Payment Risks

As domestic instant payment rails connect with international networks, bad actors exploit jurisdictional gaps, inconsistent sanctions enforcement, and differing AML standards to obscure the origin and destination of illicit funds. FedNow and RTP are currently domestic-only, but their planned linkage to SEPA Instant (EU), UPI (India), and other global systems will open new financial crime vectors that U.S. compliance teams are not yet structured to address.

Emerging risks:

- Layering funds through multiple jurisdictions within minutes via interconnected instant payment systems

- Exploiting weaker AML regimes in certain countries to mask illicit transactions

- Using cross-border instant payments to evade domestic transaction reporting thresholds

- Circumventing sanctions by routing payments through jurisdictions with limited enforcement

Building a Real-Time AML Defense: Technology and Process

Pre-Transaction Risk Scoring: The First Line of Defense

The most effective safeguard in an instant payment environment is pre-transaction risk scoring : evaluating risk before a payment initiates, not after settlement.

How it works:

Before authorizing a payment, the system evaluates:

- Sender profile — Account age, transaction history, previous fraud indicators

- Recipient identity — Known mule account, first-time payee, sanctions match

- Device signals — Location, device fingerprint, velocity anomalies

- Behavioral baseline — Does this payment match the customer's established patterns?

- Network analysis — Does the recipient share connections with known fraudulent accounts?

The system assigns a real-time risk score and routes transactions accordingly:

- Low risk → Auto-approve, settle instantly

- Medium risk → Enhanced review, brief delay, or additional authentication

- High risk → Block or escalate to investigator

The result is a compliance posture that stops high-risk payments before they settle, rather than chasing them afterward.

AI-Driven Transaction Monitoring: Cutting False Positives by 31%

Machine learning models can analyze high volumes of payment data simultaneously, identify behavioral anomalies against a customer's historical baseline, and reduce false positive rates dramatically.

A NICE Actimize case study documents a large U.S. bank that achieved:

- 31% reduction in false positive alert volumes

- 100% true positive recall (no actual suspicious activity missed)

- 1,817 investigation hours saved per quarter

- 3.5 FTEs freed to focus on high-risk activities

AI models excel at detecting patterns legacy rules miss:

- Wire stripping, where payment originators remove critical identifying information to evade screening

- Identity obfuscation through slight name, address, or account number variations used to sidestep watchlists

- Behavioral anomalies such as sudden shifts in transaction velocity, amounts, or counterparties

- Network clustering that identifies groups of accounts interacting in suspicious patterns

The Federal Reserve's synthetic identity research found that while traditional fraud models miss 85-95% of synthetic identities, ML-based tools can flag 85% , effectively inverting the detection gap. Fed white paper

Risk-Based Segmentation: Balancing Friction and Risk

Not all payments need the same scrutiny. A risk-based segmentation approach applies stricter thresholds to cross-border or high-value transfers while allowing low-value domestic payments to flow with lighter checks.

Example segmentation framework:

| Transaction Type | Risk Level | Screening Intensity |

|---|---|---|

| Domestic P2P under $500, established counterparty | Low | Light pre-transaction scoring, post-transaction sampling |

| Domestic P2P over $5,000, first-time payee | Medium | Enhanced pre-transaction scoring, real-time sanctions check |

| Cross-border instant payment | High | Full KYC verification, sanctions screening, manual review |

| Business-to-business over $100,000 | High | Multi-factor authentication, dual approval, enhanced due diligence |

Concentrating scrutiny where it matters reduces friction for everyday transactions while meeting the risk-proportionality standard FinCEN's proposed AML/CFT rule calls for.

Continuous Transaction Monitoring and Audit Trails

Segmentation strategy only works if it's backed by documentation examiners can actually audit. That means real-time logging of all flagged activity, governed by a framework that includes:

- Version-controlled rule documentation — Every monitoring rule change logged with rationale and approval

- Scenario testing — Regular back-testing of rules against known fraud patterns to validate detection rates

- Threshold reviews — Quarterly reassessment of alert thresholds as payment volumes grow

- Audit trails — Complete records of alert generation, disposition, and escalation

The Federal Reserve added fraud mitigation features to FedNow, including "account activity threshold functionality" and "correspondent net send limits," indicating the rail operator itself is adding guardrails at the network level. FedNow announcement

Cross-Functional Collaboration: Breaking Down Silos

Effective real-time AML is not a compliance-only function. Fraud prevention, cybersecurity, and AML teams must share intelligence on:

- New typologies — Emerging fraud patterns observed in production

- Mule activity — Accounts flagged by fraud teams for potential mule behavior

- Device signals — Cybersecurity indicators of account takeover or credential theft

- Sanctions updates — Real-time feeds from OFAC and other watchlist sources

Siloed teams create detection gaps. A fraud team may block a suspicious payment based on device signals while AML flags the same customer for structuring, but if those teams don't communicate, neither sees the full picture. Cross-functional case conferencing and shared alert dashboards close that gap.

The Talent Behind the Technology: Staffing for Financial Crime Compliance

Technology Is Only as Good as the People Operating It

Banks adopting real-time AML tools still need BSA officers, AML analysts, sanctions specialists, and compliance technologists who understand both regulatory requirements and the operational nuances of instant payment environments.

AI can reduce false positive rates by 31% and free 3.5 FTEs per deployment, but it cannot replace human judgment in:

- Tuning models to balance false positives and false negatives

- Investigating complex mule networks that span multiple institutions

- Interpreting ambiguous sanctions matches that require contextual judgment

- Presenting SAR filings to regulators with clear narratives and supporting evidence

- Designing governance frameworks that meet evolving regulatory expectations

The U.S. Treasury's 2026 National Money Laundering Risk Assessment explicitly warns that rapid fintech growth can "drive volume beyond the capacity of compliance staffing and controls," identifying staffing gaps as a systemic risk vector — not just an HR concern. 2026 NMLRA

The Most In-Demand Financial Crime Roles

As banks modernize financial crime programs for instant payments, specific roles are in highest demand. Each requires a distinct combination of regulatory fluency, technical literacy, and operational experience that takes years to build.

AML Investigators Fluent in AI-Assisted Alert Triage:

- Interpret ML model outputs, understand confidence scores, and escalate genuine risks

- Balance technology-driven efficiency with investigative rigor

- Provide feedback on AI-generated alerts to refine model performance

Model Risk Professionals Who Validate Transaction Monitoring Logic:

- Back-test ML models against known fraud patterns

- Document model assumptions, limitations, and validation results for examiners

- Bridge data science and compliance functions

Compliance Leaders Who Bridge Business Speed and Regulatory Rigor:

- BSA officers and CCOs who understand real-time payment operations

- Articulate risk-based frameworks to regulators and business partners

- Manage compliance in high-velocity, 24/7 payment environments

Sanctions Specialists with Real-Time Screening Expertise:

- Design customer-level sanctions screening tied to continuously refreshed watchlists

- Work across platforms like Verafin, NICE Actimize, LexisNexis, SAS, and IBM

- Manage ambiguous matches and document disposition rationale

This talent is scarce and competitive to recruit. LexisNexis reports the total annual cost of financial crime compliance in the U.S. and Canada is $61 billion — the majority of which represents labor costs. via Mayer Brown's analysis of FinCEN compliance cost data

Building Compliance Teams Requires Specialized Networks

Posting a job description is not enough. The best financial crime professionals are rarely on the market. They're already employed — often at competitors or consulting firms — and only move for the right opportunity presented by someone they trust. Reaching them requires a recruiter with deep personal networks built over years, not software scanning résumés.

Wayoh specializes in exactly this kind of search for banking and FinTech clients, placing BSA officers, compliance directors, and AML investigators across community banks, commercial banks, and payments companies. With over 10 years in the compliance and risk hiring market and 500+ professionals placed, Wayoh goes to its personal networks before ever posting a role publicly. Clients get direct access to qualified candidates who understand real-time payment environments, regulatory expectations, and the operational challenges of instant settlement.

For banks and FinTechs building or scaling financial crime compliance teams, partnering with a specialist financial services recruiter significantly accelerates access to this niche talent pool. Contact Wayoh at hiring@wayoh.co to discuss your financial crime hiring needs.

Frequently Asked Questions

What is AML in instant payment processing?

AML in instant payment processing refers to the anti-money laundering controls financial institutions must apply within the compressed settlement window of instant payment systems. These controls — real-time transaction monitoring, pre-transaction risk scoring, KYC verification, and sanctions screening — must operate fast enough to detect and prevent illicit fund movement before settlement completes.

What are common AML red flags in instant payments?

Key red flags include rapid fund dispersion across multiple accounts after receipt, transactions just below reporting thresholds (structuring), payments initiated from new accounts with thin transaction history, unusual cross-border activity, and behavior that deviates sharply from a customer's established baseline.

What are examples of instant payments?

Common U.S. instant payment systems include FedNow (launched by the Federal Reserve), The Clearing House RTP network, Zelle, and Venmo (for bank-linked transfers). Globally, systems like SEPA Instant (EU) and UPI (India) serve the same function.

How does instant payment fraud differ from traditional payment fraud?

The key difference is irrecoverability. Traditional payment systems give compliance teams time to flag and reverse suspicious transactions before funds fully disburse — instant payments settle in seconds, leaving no window for post-authorization intervention. Pre-detection is the only viable defense.

What technology do banks need for real-time AML compliance?

Effective real-time AML requires AI-driven transaction monitoring that handles high volumes with low false positives, pre-transaction risk scoring integrated with KYC data, and continuously refreshed sanctions screening. Governance tools — such as sandbox environments for testing rule changes — are equally critical before live deployment.

How should banks build their financial crime compliance teams for instant payments?

Banks should prioritize AML professionals with real-time payment experience: analysts skilled in AI-assisted alert triage, model risk specialists, and compliance leaders who balance regulatory expectations with operational speed. This is a niche talent pool, and partnering with a specialist financial services recruiter like Wayoh accelerates access to vetted candidates who already know this space.