Introduction

Many fintech compliance teams treat payment screening and transaction monitoring as interchangeable — they're not. Both are AML controls, but they operate at different stages, serve different regulatory purposes, and require different workflows. Conflating them is one of the most common and costly compliance mistakes fintechs make.

A crypto exchange might assume robust transaction monitoring eliminates the need for real-time sanctions checks. A B2B payments platform might believe screening alone satisfies BSA obligations. Both assumptions can expose the company to enforcement actions and preventable money laundering.

The distinction matters most for fintechs: high transaction volumes, real-time payment rails like RTP and FedNow, and fast growth leave little room for control gaps. Applying the wrong tool at the wrong stage can mean processing payments with sanctioned parties, missing structured layering schemes, or failing to file required SARs.

Over $4.6 billion in global AML fines were levied in 2024, with fintechs accounting for 4.3% of enforcement actions. This guide breaks down how each control works, where it applies, and how to deploy both correctly.

The United Nations Office on Drugs and Crime estimates that 2–5% of global GDP — equivalent to $800 billion to $2 trillion annually — is laundered worldwide. Every fintech handling payments is a potential conduit, which is why getting these controls right is a core business requirement, not a box-checking exercise.

TL;DR

- Payment screening checks each payment before it processes — verifying senders, receivers, and details against sanctions lists, PEP databases, and watchlists to block prohibited transactions

- Transaction monitoring watches completed transactions over time, catching behavioral patterns like structuring and layering that no single payment reveals on its own

- The core difference: screening is a pre-transaction gate; monitoring is a post-transaction lens

- Neither replaces the other — a complete AML program requires both working in tandem

- Both are mandated by FinCEN (BSA), OFAC, and FATF — gaps in either can trigger fines, enforcement actions, or lost banking partnerships

What is Payment Screening?

Payment screening (also called transaction screening) is the process of validating every transaction before approval — checking the sender, receiver, and payment details against external watchlists. These lists include OFAC's SDN list, UN consolidated sanctions, EU sanctions regimes, PEP databases, and adverse media sources.

The terms "payment screening" and "transaction screening" are used interchangeably in fintech and payments contexts. Both refer to the same pre-transaction compliance gate.

Payment screening checks for more than just name matches. It identifies:

- Sanctioned entities or jurisdictions — parties designated by OFAC, the UN, or EU for economic restrictions

- Inconsistencies with KYC data — when transaction values or counterparties conflict with onboarding risk profiles

- Geographic risk — high-risk corridors or embargoed regions

- Prohibited goods or activities — payments referencing sanctioned commodities or services

These checks make screening an active layer within the broader CDD (Customer Due Diligence) framework — one that feeds directly into onboarding decisions and ongoing risk profiles.

The Screening Process:

- Data extraction — Captures names, account numbers, transaction references, and addresses from payment instructions

- Watchlist matching — Algorithms apply fuzzy matching, phonetic matching (Soundex, Metaphone), and exact string matching to identify potential hits

- Alert generation — Flags possible matches based on configurable thresholds and risk scoring

- Review — Human analysts or rules-based logic evaluate flagged transactions

- Decision — Approve, block, or escalate to senior compliance for final determination

- Audit trail — All decisions are logged to support regulatory examination

The scale of the screening challenge is significant. The OFAC SDN list spans 3,164 pages and added 1,764 new persons in 2025 alone — which means watchlist configurations require ongoing maintenance, not just initial setup.

Use Cases of Payment Screening

Fintechs most commonly apply payment screening at:

- Customer onboarding — Initial KYC validation to prevent sanctioned parties from opening accounts

- Cross-border wire transfers — Every international payment where sender or receiver could be in a restricted jurisdiction

- Payment detail changes — When a customer adds a new beneficiary or updates account details

- High-value transactions — Payments exceeding internal or regulatory thresholds requiring enhanced due diligence

Fintech-specific scenarios where screening is critical:

- B2B payment platforms facilitating international transfers between businesses, where both sender and receiver entities must be screened against global sanctions lists

- Crypto-to-fiat conversion points where digital assets are exchanged for traditional currency, creating potential exposure to sanctioned wallets or individuals

- Lending platforms disbursing funds to new recipients, where the borrower or repayment account holder could be a prohibited party

What is Transaction Monitoring?

Transaction monitoring is the ongoing, post-transaction surveillance of customer financial activity — designed to detect patterns and behavioral anomalies that indicate money laundering, terrorist financing, or fraud.

Screening examines individual transactions in isolation. Monitoring evaluates the broader picture of customer behavior over time.

Key red flags transaction monitoring systems detect:

- Structuring — Breaking large sums into smaller transactions below $10,000 reporting thresholds to evade CTR filing

- Rapid fund transfers — Moving money quickly across multiple accounts or jurisdictions (layering)

- Dormant account spikes — Previously inactive accounts suddenly showing high transaction volumes

- Profile inconsistencies — Activity that contradicts the customer's declared business, income source, or geographic location

- Layering schemes — Using seemingly legitimate intermediaries to obscure illicit fund origins

How Transaction Monitoring Systems Work:

Modern monitoring combines rule-based thresholds with AI/ML behavioral analytics. Most systems follow a five-stage workflow:

- Rules-based logic flags transactions meeting specific criteria — daily aggregates over $10,000, velocity spikes exceeding 200% of baseline, or geographic patterns matching known typologies

- Behavioral models establish each customer's normal activity baseline and surface statistical deviations, reducing false positives that rigid thresholds alone produce

- Alert triage routes flagged transactions into investigative queues, prioritized by risk score and alert type

- Analyst review determines whether flagged activity is explainable or warrants escalation to a supervisor or compliance officer

- SAR filing occurs within 30 days when suspicious activity is confirmed, as required by FinCEN regulations

Effective monitoring depends on full context. KYC/KYB onboarding data, past transaction history, screening results, and risk scoring all feed into better-calibrated rules. Without that context, systems generate excessive false positives — a well-documented problem at institutions where 90-95% of alerts turn out to be benign.

That alert fatigue problem is exactly where fintech-specific scenarios get instructive.

Use Cases of Transaction Monitoring

Fintech-specific transaction monitoring scenarios:

- Neobank detecting smurfing — A customer suddenly receives dozens of small peer-to-peer transfers from different users, followed by rapid outflows to external accounts (classic structuring indicator)

- Lending platform routing detection — A borrower makes repayments through multiple third-party accounts rather than their registered bank account, suggesting potential money laundering or identity fraud

- Crypto exchange structuring — A wallet makes repeated deposits just under reporting thresholds ($9,500, $9,800) across multiple days, a red flag for deliberate avoidance of CTR filing

None of these scenarios would surface from a single transaction review. Each one only becomes visible when the system looks across weeks of activity — which is why fintech compliance teams need monitoring calibrated to their specific product flows, not generic bank rules copied from legacy playbooks.

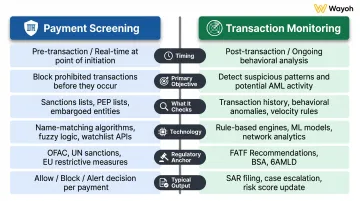

Payment Screening vs Transaction Monitoring: Key Differences Explained

| Dimension | Payment Screening | Transaction Monitoring |

|---|---|---|

| Timing | Pre-transaction, real-time (before payment clears) | Post-transaction, ongoing (after payment completes) |

| Primary Objective | Prevent prohibited parties from transacting | Detect suspicious behavioral patterns over time |

| What It Checks | Names, entities, jurisdictions against sanctions/PEP/watchlists | Behavioral anomalies, transaction patterns, profile deviations |

| Technology | Fuzzy/phonetic/NLP name-matching algorithms | Rule-based thresholds + AI/ML behavioral models |

| Regulatory Anchor | OFAC/UN/EU sanctions compliance (31 CFR Part 501) | BSA, FATF Recommendations 10 & 20, SAR filing obligations (31 CFR Chapter X) |

| Enforcement Agency | OFAC (strict liability) | FinCEN (willfulness standard) |

| Typical Output | Block, approve, or escalate payment | Investigate, document, file SAR if warranted |

The Substitution Misconception

Transaction monitoring is not a substitute for payment screening. A customer who passes KYC onboarding and looks clean in a monitoring system can still be a sanctioned entity — only a real-time sanctions check at the payment level catches this. Screening alone, conversely, cannot detect laundering through structuring or layering; that's exactly what monitoring is built for.

Enforcement actions illustrate both failure modes. BitPay's $507,375 OFAC penalty for processing 2,102 transactions with sanctioned jurisdictions shows the cost of screening gaps. Robinhood Crypto's $30 million NYDFS fine for inadequate transaction surveillance shows what happens when monitoring falls short.

How Screening and Monitoring Connect

Screening data and results feed directly into the monitoring system's risk context. A transaction flagged and cleared during screening should be tagged as elevated-risk for ongoing scrutiny — this integration is what separates a siloed AML approach from a mature one.

When a B2B payments platform screens a new beneficiary and finds a partial name match requiring manual review, that context should carry forward into monitoring rules. Future transactions with that entity warrant lower alert thresholds precisely because the risk signal already exists.

The False Positive Problem Differs Structurally

- Screening: False positives come from name-matching ambiguity — aliases, transliterations (Mohammad vs. Mohammed), partial matches (John Smith against thousands of records), and common names. Mitigations include fuzzy matching tolerance tuning, phonetic algorithms (Soundex, Metaphone), and continuous list updates.

- Monitoring: False positives come from overly broad rules — flagging every high-value transfer regardless of customer profile, rigid velocity thresholds that ignore business cycles, or geographic rules that don't account for legitimate cross-border activity. Mitigations include behavioral profiling, AI-driven alert prioritization, and dynamic baselines.

Industry research shows 90-95% of AML transaction monitoring alerts are false positives, consuming analyst time and driving $61 billion in annual compliance costs across the United States and Canada. For fintech compliance teams, reducing that false positive rate is one of the highest-leverage investments in both analyst capacity and regulatory credibility.

Why Fintech Teams Need Both

The layering scheme blind spot illustrates why neither tool alone is sufficient. A money launderer using a "clean" legal entity or newly onboarded individual will pass screening because there's no sanctions match. But transaction monitoring will eventually detect the unusual pattern of fund flows — small incoming transfers from dozens of sources, rapid consolidation, and immediate outbound wires to high-risk jurisdictions. Without monitoring, screening-only fintechs are exposed to sophisticated laundering. Without screening, monitoring-only fintechs risk processing sanctioned party transactions before any pattern is detectable.

Regulatory and Business Risk of Gaps

Regulators explicitly require both controls. FATF Recommendation 6 mandates targeted financial sanctions (screening), while Recommendation 20 separately requires suspicious transaction reporting (monitoring) — these are distinct obligations under different legal frameworks. FinCEN issued $3.4 billion in civil penalties in FY2024, dominated by Binance's record-breaking settlement for BSA/AML program failures.

For fintechs that rely on partner banks for deposit accounts, payment processing, or card issuing, losing that banking sponsor relationship is an existential risk. Banks terminate fintech partnerships when AML programs fall short — and that threat is well understood across the industry, even when specific cases remain confidential.

The Talent Reality

Running both programs requires skilled compliance professionals — analysts who can tune rules, review alerts, conduct investigations, and file SARs accurately. As fintechs scale, the complexity of these programs outgrows tooling alone.

A neobank processing 100,000 transactions monthly might start with off-the-shelf software. By 500,000 transactions, they need professionals who understand regulatory expectations, can calibrate thresholds to their specific risk profile, and can defend their methodology to examiners.

That talent gap is where programs break down — and where Wayoh focuses. The firm has placed BSA Officers, AML Analysts, and Chief Compliance Officers at payments companies, neobanks, and crypto platforms — the exact environments where screening and monitoring programs must scale alongside transaction volume. Technology sets the floor; the people running it determine whether the program actually holds up to examiner scrutiny.

Conclusion

Payment screening and transaction monitoring serve different functions, but they belong together in any complete AML program. Screening blocks known bad actors before a transaction clears. Monitoring catches unknown patterns after transactions occur. Both are necessary — neither substitutes for the other.

As real-time payment adoption accelerates — with the RTP network reaching 950+ institutions and FedNow enrolling 1,600+ participants — both programs must keep pace through better tooling, updated rules, and critically, experienced AML professionals who know how to adapt these controls as the regulatory landscape shifts. The right hire in a BSA, sanctions, or transaction monitoring role is often what separates a defensible program from a regulatory action — and that's where firms like Wayoh, which specializes in placing AML and financial crime professionals across fintech and banking, can make a direct difference.

Frequently Asked Questions

What is the difference between payment screening and transaction monitoring?

Payment screening checks transactions before they are processed against sanctions lists and watchlists to block prohibited parties, while transaction monitoring analyzes completed transactions over time to detect suspicious behavioral patterns like structuring or layering. Screening is a real-time gate; monitoring is ongoing surveillance.

What is the purpose of payment screening?

Payment screening's primary purpose is to prevent transactions involving sanctioned individuals, entities, or jurisdictions from being processed, serving as a real-time compliance gate. It also supports KYC/CDD requirements under AML regulations by verifying counterparties at the point of transaction.

Is payment screening the same as transaction screening?

Yes, payment screening and transaction screening are used interchangeably. Both refer to the pre-transaction process of checking payment details against sanctions, PEP, and watchlists, with "payment screening" more common in fintech and payments contexts.

When is a fintech legally required to implement transaction monitoring?

Fintechs subject to BSA obligations (Money Services Businesses, banks, and broker-dealers) must implement transaction monitoring under FinCEN regulations, with FATF recommendations extending similar expectations globally. The obligation typically triggers once a fintech handles customer funds or facilitates payments.

What are the most common red flags in transaction monitoring for fintechs?

Common red flags include structuring (breaking transactions below reporting thresholds), rapid fund movement across accounts or jurisdictions, activity inconsistent with a customer's declared risk profile, and sudden spikes in transaction volume from previously dormant accounts.

What happens if a fintech fails to implement AML payment screening or transaction monitoring?

Consequences range from FinCEN and OFAC fines to loss of banking sponsor relationships, reputational damage, and criminal liability for individuals. Penalties can reach into the billions — FinCEN's 2023 settlement with Binance totaled $3.4 billion.