Introduction: Why KYC Identity Management Is Now a Hiring Priority

Compliance functions at banks and fintechs are under more pressure than they've been in years. Regulatory enforcement is intensifying—FinCEN assessed a record $1.3 billion penalty against TD Bank in October 2024, part of a $3.09 billion global resolution. FinCEN Director Andrea Gacki attributed the failure directly to a compliance program allowed to "languish" for over a decade — a staffing and budget failure with a ten-figure price tag.

Meanwhile, digital transformation is creating demand for KYC professionals who understand not just the regulatory framework but also the identity verification tools, API-driven platforms, and automated monitoring systems that modern compliance programs run on. That combination of regulatory depth and technology fluency is scarce — and getting scarcer as more organizations compete for the same narrow pool of qualified professionals.

This guide covers what hiring managers need to know: the foundations of KYC identity management, the roles that belong on a modern compliance team, what to evaluate when hiring, and why qualified KYC talent is harder to find than most organizations expect.

Key Takeaways

- KYC identity management spans three core functions: Customer Identification (CIP), Due Diligence (CDD/EDD), and Ongoing Monitoring

- Every U.S. financial institution—including fintechs—is legally required to maintain a KYC program under the Bank Secrecy Act and USA PATRIOT Act

- Four roles drive most KYC programs: KYC Analyst, Compliance Officer, IDV Specialist, and BSA/AML Operations Lead

- CAMS, CFCS, and CFE certifications are the strongest proxy for baseline competency in mid-to-senior hires

- 57% of AML professionals report concerns about staffing adequacy, and the talent shortage shows no signs of self-correcting

What Is KYC Identity Management—and Why It Matters in Banking and Fintech

Know Your Customer (KYC) is the regulatory requirement that obligates financial institutions to verify customer identities, assess risk profiles, and monitor behavior throughout the customer lifecycle. It doesn't stop at onboarding—it's an ongoing obligation.

Identity management is the operational layer that makes KYC actionable. Document checks, biometric verification, database screening, and sanctions list lookups are the tools that turn regulatory requirements into repeatable, auditable workflows. When these functions align, institutions can demonstrate exam-ready compliance, manage onboarding risk by customer tier, and detect suspicious activity before it becomes a reporting failure.

The Regulatory Foundation

Two federal laws establish the KYC obligation for U.S.-regulated institutions—with a third rule closing the gaps they left open:

- Bank Secrecy Act (BSA) — requires recordkeeping, reporting of cash transactions exceeding $10,000, and filing Suspicious Activity Reports (SARs) when criminal activity is suspected

- USA PATRIOT Act, Section 326 — established the Customer Identification Program (CIP) requirement, setting minimum identity verification standards before any business relationship begins

- FinCEN's Customer Due Diligence (CDD) Rule (2016) — added the beneficial ownership requirement, obligating covered institutions to identify and verify the natural persons who own or control legal entity customers

These laws apply to banks, credit unions, broker-dealers, anddirectly to money services businesses, a category that captures many fintech payment platforms and lenders. The assumption that fintech companies operate outside BSA/AML obligations is wrong, and regulators have made that clear through enforcement.

The cost of non-compliance isn't theoretical. Capital One paid $390 million to FinCEN in 2021 for willful BSA violations. TD Bank's 2024 resolution was nearly eight times larger. For compliance and risk leaders, these cases signal where regulatory scrutiny is headed—and what staffing gaps can cost.

The Three Pillars of KYC That Every Compliance Team Operates Around

Every KYC professional a bank or fintech hires will be expected to understand and operate within a three-part framework. Knowing how candidates engage with each pillar tells you more about their practical competence than a credential list ever will.

Customer Identification Program (CIP)

CIP is the first gate. Before a business relationship begins, institutions must collect and verify four categories of identity information:

- Full legal name

- Date of birth

- Address (residential or business)

- Identification number (SSN for U.S. persons; passport number or equivalent for non-U.S. persons)

Under 31 CFR 1020.220, this program must be written, integrated into the institution's AML compliance program, and use risk-based procedures for verification. "Risk-based" matters here: the depth of verification required scales with the risk the customer presents.

Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD)

CDD is the risk-profiling layer. Under FinCEN's CDD Final Rule, covered institutions must:

- Identify and verify customers and beneficial owners of legal entity customers (anyone owning 25% or more of equity interests)

- Understand the nature and purpose of customer relationships

- Assign risk tiers and maintain customer risk profiles

- Escalate high-risk accounts to Enhanced Due Diligence (EDD)

EDD requires deeper investigation: source of funds documentation, PEP (politically exposed person) screening, and sanctions list checks. A 2020 interagency joint statement from FinCEN, the Federal Reserve, FDIC, NCUA, and OCC clarified that not all PEPs carry the same risk level—institutions should apply a risk-based approach rather than blanket de-risking.

Errors at the CDD stage—under- or over-classifying risk—are among the most common findings during regulatory examinations. Candidates who can articulate how they've handled risk tier decisions are worth prioritizing.

Ongoing Monitoring

Compliance doesn't conclude at account opening. Ongoing monitoring includes:

- Transaction surveillance against behavioral baselines

- Periodic customer re-verification

- Watchlist re-screening as lists are updated

- SAR filing when thresholds are triggered (banks must file within 30 calendar days of identifying suspicious activity)

Much of this is now automated. But automation doesn't eliminate the need for human judgment; it concentrates it. Someone still has to investigate alerts, decide which SARs to file, and catch what the system misses. That judgment is a core hiring criterion, not an optional skill.

Key Roles Within a KYC and Identity Management Function

Most banks and fintechs need defined coverage across four functional areas to run a compliant identity management program. The right org structure varies by institution size, but these roles form the foundation.

KYC Analyst

The core operational role. KYC Analysts review customer documentation, complete due diligence questionnaires, resolve discrepancies, and escalate high-risk cases. This is typically an entry-to-mid-level position and is among the most in-demand hires for growing fintechs.

What to expect from candidates:

- Familiarity with CIP workflows and watchlist screening tools

- Hands-on experience with case management systems

- Judgment to escalate appropriately — without defaulting to blanket escalations that slow operations

KYC/AML Compliance Officer

Compliance Officers write and maintain KYC policies, liaise with regulators, oversee BSA/AML audits, and train staff. The role demands demonstrated experience with regulatory examinations and a working knowledge of FinCEN, OCC, and FDIC expectations — not just the terminology.

Senior Compliance Officers typically command $100,000–$150,000+, per Robert Half's 2026 data. Budget planning should reflect that this hire is compensation-competitive.

Identity Verification (IDV) Specialist or Manager

IDV Specialists sit at the intersection of compliance and product — configuring identity verification platforms, setting document verification rules, and collaborating with engineering on onboarding flows. This role emerged directly from fintech's digital-first model.

Candidates need both compliance knowledge and comfort with API-driven tools and RegTech platforms. Few professionals have developed both skill sets organically, which makes this one of the harder roles to fill.

BSA/AML Operations Lead

Operations Leads manage queue workflows, track SLAs, supervise analyst teams, and own process improvement. For institutions scaling their compliance teams, this hire is what separates clean growth from accumulated backlogs and quality gaps.

Demand spans all four role types — from analysts and specialists through BSA Officers and Chief Compliance Officers. Interim placements frequently fill urgent gaps during audits, remediation projects, or rapid growth periods. Guided by a human-first recruiting approach, Wayoh has placed professionals across each of these roles for banks and fintechs in New York, California, Florida, and other major U.S. markets for over 3 years.

What to Look for When Hiring KYC Identity Management Professionals

A mis-hire in a compliance role carries two costs: regulatory exposure during the gap, and the time and expense of a replacement search. These evaluation criteria help hiring managers avoid both.

Technical Knowledge of Regulatory Frameworks

Prioritize candidates who can articulate how BSA, the USA PATRIOT Act, FinCEN CIP/CDD guidance, and OFAC sanctions requirements translate into daily workflow decisions. Listing regulations on a resume is not the same as understanding how to apply them.

Ask candidates to walk through how they'd handle a specific scenario—a beneficial ownership discrepancy, a customer with a PEP connection, a watchlist hit on a name with multiple common variations.

Hands-On Experience with KYC and IDV Platforms

Tool fluency is an increasingly meaningful differentiator. Ask candidates to describe specific platforms they've used and how they've configured or worked within them:

- Identity verification platforms (document capture, biometric matching)

- Case management and workflow systems

- Watchlist and sanctions screening tools

- Transaction monitoring software

Candidates who can speak to configuration decisions, not just platform familiarity, have hands-on ownership experience that translates directly to faster ramp time and fewer compliance gaps.

Analytical Judgment and Risk Reasoning

Strong KYC professionals make risk-based decisions in ambiguous situations with incomplete data. The best behavioral interview questions probe real decisions:

- How did you handle a borderline EDD case where the documentation was technically complete but the risk profile felt off?

- Describe a SAR decision where you disagreed with the initial assessment

- How have you managed a documentation gap during onboarding without defaulting to outright rejection?

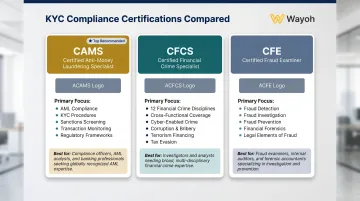

Certifications as a Proxy for Baseline Competency

Three credentials anchor the KYC hiring market:

| Certification | Issuing Body | Primary Focus |

|---|---|---|

| CAMS (Certified Anti-Money Laundering Specialist) | ACAMS | AML, KYC, sanctions, transaction monitoring |

| CFCS (Certified Financial Crime Specialist) | ACFCS | 12 financial crime areas; cross-functional |

| CFE (Certified Fraud Examiner) | ACFE | Fraud detection, investigation, prevention |

CAMS is the most widely recognized for KYC/AML roles. Treat it as a strong signal for mid-to-senior hires, not a strict requirement for every position. Specifying "preferred vs. required" in job postings keeps the candidate pool appropriately wide.

Communication and Cross-Functional Collaboration

KYC professionals regularly work across product, engineering, legal, and business teams, especially in fintech environments. The ability to translate a regulatory requirement for a product manager — without over-legalizing it or understating the risk — is a real and distinguishable skill.

Test it in the interview. Listen not just to how candidates talk about compliance, but how they frame it for non-compliance audiences. That distinction separates strong communicators from technically sound but operationally isolated hires.

Why Finding Qualified KYC Talent Is Harder Than It Looks

The numbers tell a clear story. According to an ACAMS survey, 57% of AML professionals are concerned about having enough properly trained staff—up from 36% in 2013. Around 26% identify staffing as their single greatest challenge.

Meanwhile, the BLS projects only 3% employment growth for compliance officers through 2034. The 33,300 annual openings projected each year are primarily replacement-driven. There is no surge of qualified candidates on the horizon.

Why Broad Sourcing Doesn't Work for KYC

When institutions post KYC roles on general finance job boards, several problems emerge:

- Active candidates dominate responses; experienced practitioners are often passive

- Screening without compliance expertise produces mis-hires before candidates reach interviews

- Time-to-fill extends as teams sift through volume rather than quality

- The cost of a wrong hire in a regulated function is measured in both salary and regulatory exposure

LexisNexis found that labor represents approximately 70% of total financial crime compliance costs for U.S. and Canadian institutions—totaling an estimated $61 billion annually. At that scale, every mis-hire or extended vacancy carries direct financial exposure—making candidate quality a budget concern, not just a hiring one.

The Case for Compliance-Specialized Recruiting

Specialized recruiting firms like Wayoh approach this differently. With 10+ years and 500+ placements across banks, fintechs, and regulated institutions, Wayoh's network-first model targets both active and passive candidates—including experienced compliance professionals who aren't responding to job postings but can be reached through direct market relationships.

For KYC-specific searches, that reach matters. Interim placements can cover immediate needs during audits or remediation projects while permanent searches run in parallel. This dual-track structure prevents compliance gaps from widening during extended hiring cycles.

Frequently Asked Questions

What is KYC in identity verification?

KYC (Know Your Customer) is the process by which financial institutions confirm a customer's identity using government-issued documents, biometrics, and database checks—before and throughout the business relationship. It establishes that the person is who they claim to be and supports ongoing risk assessment.

What are the main steps of the Customer Identification Program (CIP)?

CIP requires collecting four pieces of identity information—name, date of birth, address, and ID number—then verifying that information against reliable source documents or databases. Institutions must retain CIP records to demonstrate compliance during regulatory examinations.

Is KYC mandatory in the USA?

Yes. KYC is mandatory for U.S. financial institutions under the Bank Secrecy Act and the USA PATRIOT Act, enforced by FinCEN, the OCC, the FDIC, and other regulators. Non-compliance can result in substantial civil and criminal penalties, including nine-figure fines.

Is KYC verification legitimate?

KYC verification is a legally required process. Reputable institutions collect identity information to meet regulatory obligations, and all data is subject to strict privacy and security standards under federal law.

What certifications are most valued for KYC compliance roles?

CAMS (Certified Anti-Money Laundering Specialist) is the most widely recognized, followed by CFCS and CFE. For mid-to-senior compliance hires, these credentials signal solid foundational knowledge—though they're not always a hard requirement across every KYC role.

How long does it typically take to hire a qualified KYC professional?

KYC and AML searches typically run longer than general finance roles given the specialized regulatory knowledge required. Working with a compliance-focused recruiter who maintains active candidate networks can meaningfully shorten time-to-fill.