The message is clear: compliance leadership in banking and fintech isn't a back-office function anymore. A weak or mismatched CCO hire exposes your firm to enforcement action, examination failures, and personal liability for the individuals involved.

This guide covers what a banking or fintech CCO actually does, how to identify the right candidate profile, where to find them, and how to structure the hiring process — including compensation benchmarks and reporting structure decisions that regulators pay attention to.

Key Takeaways

- A banking or fintech CCO owns the CMS, manages examiner relationships, and carries personal liability for BSA/AML program governance

- Prioritize domain-specific experience in banking or fintech regulation, not just general compliance; look for CRCM, CAMS, or relevant certifications

- Source through compliance-specialized recruiters, regulatory alumni networks, and professional associations rather than general job boards

- Evaluate via regulatory scenario interviews and reference checks that reach beyond the candidate's provided list

- Structure the CCO to report to the CEO or board (not Legal), and set compensation benchmarks before going to market

Why Banking and Fintech CCO Hiring Demands a Specialized Approach

Banking and fintech operate under a regulatory stack that most compliance professionals in other industries have never touched. The core frameworks alone — BSA/AML, TILA, RESPA, UDAAP, Reg Z, Reg E, OFAC screening — represent years of specialized experience. Add to that the state-level complexity: 49 states regulate money transmission, creating a fragmented, ongoing licensing burden that a healthcare or insurance compliance background simply doesn't prepare someone for.

A generalist CCO faces a steep and costly learning curve. By the time they get up to speed, your next examination may already be scheduled.

Fintech Adds Another Layer

Fintechs often operate across dozens of state licenses simultaneously, partner with sponsor banks under Banking-as-a-Service (BaaS) arrangements, and face heightened CFPB scrutiny.

The 2024 CFPB final rule on general-use digital consumer payment apps brought qualifying nonbanks under formal supervision for the first time. That means a fintech without dedicated compliance leadership is now exposed to the same examination risk as a bank — not a role you can hand to a dual-hatted executive.

The right fintech CCO needs to understand startup velocity and the regulatory weight of a chartered bank. Few candidates have operated credibly on both sides of that line, which is exactly why the search takes longer and generic job postings rarely surface the right person.

Examiner Interaction Is a Core Competency

In banking, the CCO may sit across the table from OCC, FDIC, or Federal Reserve examiners during safety-and-soundness exams. This requires someone who has either come from a regulatory agency or has extensive direct examiner interaction experience — not someone who has only read the handbooks.

What a CCO Actually Does in Banking and Fintech

Many hiring managers underestimate the scope. The CCO role in a regulated financial institution covers at least five distinct functions:

Owning the Compliance Management System

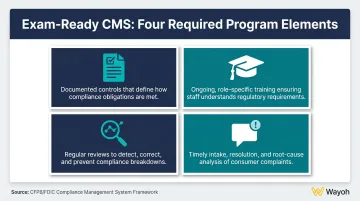

The CFPB and FDIC define a CMS around two components and four program elements:

- Written policies and procedures

- Compliance training

- Monitoring and testing

- Consumer complaint response

An exam-ready CMS requires documented outcomes across all four pillars. The CCO is accountable for building, maintaining, and demonstrating each one.

Regulatory Relationship Management

The CCO is the primary point of contact with bank examiners and regulatory agencies. Key responsibilities here include:

- Managing responses to Matters Requiring Attention (MRAs) and Matters Requiring Immediate Attention (MRIAs)

- Coordinating exam preparation and documentation

- Overseeing state licensing renewals across multiple jurisdictions (especially critical in fintech)

Product and Business Advisory

In fintech especially, the CCO evaluates new products and features before launch, partners with legal and product teams to flag compliance risks early, and keeps the business moving rather than stopping it. Firms that treat compliance as an afterthought typically move slower and face more regulatory friction than those who bring the CCO into the product development process from the start.

BSA/AML Program Ownership

Banks must designate an individual responsible for day-to-day BSA/AML compliance under 31 CFR 1020.210, covering internal controls, independent testing, training, and risk-based customer due diligence. The CCO often serves as — or directly oversees — the BSA Officer.

The personal stakes here are real. FinCEN assessed a $450,000 personal penalty against a former U.S. Bank official for willful BSA program failures. This is not a role where gaps in ownership go unnoticed.

Board and Executive Reporting

The CCO reports compliance program status directly to the board or board audit/risk committee. That makes executive communication skills non-negotiable. Specifically, the right candidate must be able to:

- Translate regulatory risk into business language directors can act on

- Present program gaps and remediation timelines without burying the lead

- Build credibility with non-compliance stakeholders at the highest level of the organization

Key Qualifications and Qualities to Look for in a CCO

Credentials and Domain Expertise

Start with demonstrated experience in banking or fintech regulatory environments specifically — not just "financial services compliance."

Preferred backgrounds:

- Current or former compliance officer at a bank, thrift, credit union, or licensed fintech

- Former regulatory agency examiner (OCC, CFPB, FDIC, Federal Reserve)

- BSA/AML program builders with documented exam outcomes

Relevant certifications:

- CRCM (Certified Regulatory Compliance Manager) — the ABA's standard for U.S. banking compliance professionals

- CAMS — ACAMS counts 65,000+ certificants; essential for BSA/AML-heavy roles

- CIPP — valuable for fintechs with significant data privacy exposure

Assess depth by asking candidates to walk through the specific regulations governing your business model. For a consumer lender: TILA/Reg Z, RESPA, FCRA, UDAAP. For a payments fintech: Reg E, state MSB laws, FinCEN guidance on virtual currency. Candidates who can only name regulations — without explaining how they apply to your specific model — are a red flag.

Leadership and Organizational Authority

A CCO who also carries General Counsel, CFO, or COO responsibilities cannot give compliance the attention regulators expect. Dual-hatting is exactly the structural weakness that draws examiner criticism — and one of the first things agency reviewers flag.

The CCO must be willing to escalate uncomfortable findings to the board — even when leadership doesn't want to hear them. During interviews, ask directly: Tell me about a time you delivered a compliance finding that senior management pushed back on. What did you do? The answer reveals far more than credentials do.

Adaptability and Technology Fluency

Regulations shift, and so do enforcement priorities. Strong candidates will demonstrate:

- Awareness of emerging frameworks (AI governance, CFPB open banking rules, evolving crypto regulations)

- Comfort with regtech tools for transaction monitoring, policy management, and exam management

- Ability to build compliance programs that scale — not just maintain existing ones

How to Source and Recruit a Banking or Fintech CCO

Why Standard Channels Fall Short

General job boards and LinkedIn keyword searches produce volume, not quality. Verifying regulatory knowledge, examiner relationships, and industry-specific track records requires time and context that automated matching can't provide.

The strongest CCO candidates are already employed in senior roles and won't respond to a public job posting. If your search strategy depends on inbound applications, you're missing most of the available talent.

Effective Sourcing Channels

| Channel | What It Surfaces |

|---|---|

| Regulatory alumni networks | Former OCC, CFPB, and Fed examiners transitioning to industry |

| ACAMS and ABA Compliance School networks | Active practitioners with documented credentials |

| Compliance-specialized executive search firms | Passive senior candidates not visible on job boards |

| Direct referrals from board members or counsel | Trusted candidates with existing credibility |

Firms like Wayoh — which focus exclusively on compliance, risk, and legal hiring in banking and fintech and operate from a human-first recruiting philosophy — can compress the search timeline by surfacing passive candidates through direct outreach and long-term market relationships built over 10+ years in financial services.

The Case for Confidential Search

Many CCO searches happen while an incumbent is still in place, or under circumstances where a public posting would signal instability. A relationship-led search process — where a recruiter engages candidates through trusted networks without a public listing — is often the only way to access senior talent discreetly without disrupting your organization or tipping off competitors.

Build a Specific Job Description

Vague job descriptions attract mismatched candidates. A strong CCO posting should include:

- Regulatory footprint: Which agencies, which regulations, which states

- Reporting structure: Does the CCO report to the CEO, board, or GC?

- Team scope: How many direct reports, what functions does the role own?

- BSA/AML specifics: Is the CCO also the designated BSA Officer?

A precise, role-specific description also signals to qualified candidates that leadership understands what the job actually requires — which matters when you're competing for senior talent already fielding multiple approaches.

Compensation Benchmarks and Reporting Structure

What to Budget

CCO compensation in banking and fintech varies significantly by firm size, charter type, and geography. Typical ranges break down as follows:

- Community banks under $1B in assets: Base salaries typically range from the mid-$100Ks to low-$200Ks depending on market and scope

- Mid-size regional banks: Base compensation generally in the $200K–$350K range, with discretionary bonus

- Growth-stage fintechs: Competitive base plus equity participation, particularly for Series B+ companies under active regulatory scrutiny

The ABA reported average banking base salary increases of 4.2% in 2024 — competition for qualified compliance talent has only intensified since. For current tiered benchmarks by role and asset size, obtain data from the ABA Compensation Survey, Aon/Radford, Pearl Meyer, or Mercer before going to market. Entering a search without current data leads to losing candidates at the offer stage.

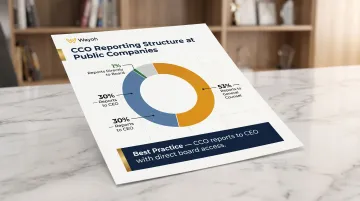

The Reporting Structure Question

Where the CCO sits in your org chart signals compliance culture to regulators.

Industry data shows 53% of public-company CCOs report to the General Counsel, with only 30% reporting to the CEO and 1% reporting directly to the board. Regulators still push hard for board oversight and independent authority for the compliance function — it's a recurring theme in Compliance Management System (CMS) examination guidance.

A CCO who reports to Legal faces a real independence problem. When the GC also advises on deals and transactions, compliance priorities get crowded out by commercial ones.

Best practice:

- CCO reports to the CEO

- CCO has direct, regular access to the board audit or risk committee

- CCO has independent authority to escalate findings without management filter

Firms where the CCO has a seat at the senior leadership table perform better in regulatory examinations than those where compliance is buried under Legal or Operations.

Frequently Asked Questions

How much does a Chief Compliance Officer make in the US?

CCO salaries in banking and fintech range broadly — from the mid-$100Ks at smaller community banks to $400K+ total compensation at large regional banks or well-funded fintechs. Total comp typically includes base salary plus discretionary bonus, and equity for fintech roles. Current benchmarks are available through the ABA Compensation Survey, Aon/Radford, or Pearl Meyer.

Can the CEO fire the Chief Compliance Officer?

Yes, the CEO typically has termination authority over the CCO. This is exactly why CCO independence and direct board access matter: a CCO without board involvement in removal decisions has limited ability to escalate findings that conflict with executive preferences. Some institutions build procedural protections around CCO termination to prevent retaliation for compliance escalations.

What are the 7 pillars of compliance?

The seven pillars are written standards and policies, training and education, oversight and accountability, communication, auditing and monitoring, enforcement, and response and prevention. A strong CCO candidate should demonstrate hands-on experience building each pillar — not just describe them conceptually.

When should a fintech startup hire its first dedicated CCO?

Key triggers: entering CFPB supervision as a larger participant, registering as an MSB with FinCEN, pursuing multi-state money transmission licensure, or entering a bank partnership under a BaaS arrangement. If a dual-hatted executive is managing compliance alongside other responsibilities and you're scaling, it's already time.

What is the difference between a CCO and a Chief Risk Officer in banking?

The CCO focuses on regulatory compliance — laws, rules, and regulatory expectations — including the CMS and BSA/AML program governance. The CRO oversees enterprise risk, including credit, market, liquidity, and operational risk. Larger banks maintain both as distinct roles; smaller institutions sometimes combine them, though regulators generally prefer dedicated compliance leadership.