Introduction

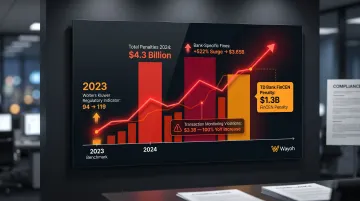

U.S. regulatory enforcement is tightening — and the numbers reflect it. Penalties across federal regulators hit $4.3 billion in 2024, with bank-specific fines surging 522% to $3.65 billion. FinCEN's record $1.3 billion penalty against TD Bank made one thing plain: program-level compliance failures don't just cost money — they threaten a bank's operating license.

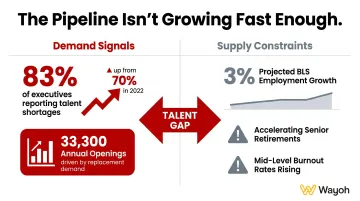

Those stakes make compliance hiring more consequential than ever — and harder. Demand for qualified compliance professionals is outpacing supply. The BLS projects only 3% employment growth for compliance officers over the next decade — yet roughly 33,300 positions open annually just from replacement demand. Retirement, burnout, and specialization gaps are leaving institutions exposed at exactly the wrong time.

This guide covers the regulatory landscape driving that demand, the roles institutions need to fill, and what to prioritize when hiring compliance leaders who can keep your institution out of an enforcement action.

Key Takeaways

- Federal and state regulations (SOX, GLBA, BSA/AML, CCPA, 23 NYCRR 500) create distinct compliance hiring needs across financial institutions

- Non-compliance carries real costs: fines, enforcement actions, reputational damage, and examiner scrutiny

- Key compliance roles — CCO, BSA/AML Officer, Fair Lending Specialist — demand specialized expertise that varies significantly by function

- The strongest compliance hires combine credentials (CRCM, CAMS) and examiner experience with genuine leadership ability

- In a tight talent market, working with a specialized recruiter provides access to passive candidates that job postings won't reach

What Is Financial Regulatory Compliance, and Why Does It Keep Escalating?

Financial regulatory compliance is the set of systems, policies, and practices institutions use to meet legal and ethical standards — covering consumer protection, data security, anti-money laundering, capital requirements, and more. It's not a single framework. It's a layered, overlapping set of obligations enforced by multiple agencies with distinct mandates.

The Federal Oversight Structure

| Agency | Primary Oversight Focus |

|---|---|

| OCC | National banks and federal savings associations |

| FDIC | State-chartered non-member banks and all insured depositories |

| CFPB | Consumer financial law enforcement for banks over $10B and non-bank providers |

| SEC | Public companies, broker-dealers, and investment advisers |

| FINRA | Broker-dealer firms and registered representatives |

State regulators layer on top of this. New York's DFS, California's DFPI, and others have advanced their own requirements — often with stricter standards than federal minimums — creating a patchwork burden for any multi-state institution.

Why the Burden Keeps Growing

The Wolters Kluwer Regulatory & Risk Management Indicator rose to 119 in 2023, a 25-point jump from 94 the prior year — the sharpest single-year escalation in the survey's history. Since the 2008 financial crisis, regulatory volume has expanded steadily, and enforcement intensity has followed. Transaction monitoring violations alone generated $3.3 billion in penalties in 2024 — a 100% year-over-year increase.

Each new regulation, enforcement action, or agency guidance creates immediate demand for someone qualified to own it. That's why experienced compliance professionals have become among the most competed-for hires in financial services.

Key Regulations Driving Compliance Hiring Demand

SOX and GLBA

Sarbanes-Oxley (SOX) requires CEO and CFO quarterly certification of financial disclosures (Section 302) and annual management assessment of internal controls over financial reporting (Section 404). IT access controls, audit trails, and financial record retention all fall within scope. Institutions need compliance professionals who understand both financial governance and technology security requirements.

GLBA's Safeguards Rule, updated in June 2023, requires financial institutions to designate a qualified individual to oversee their information security program, implement access controls and multi-factor authentication, and report security breaches to the FTC within 60 days. A May 2024 amendment extended breach notification obligations to non-banking financial institutions.

BSA/AML

The Bank Secrecy Act requires every bank to maintain a formal AML program built on four pillars:

- Internal controls governing transaction monitoring and recordkeeping

- Independent testing of AML program effectiveness

- A designated BSA compliance officer with clear accountability

- Ongoing employee training across relevant business lines

The filing burden is substantial — FinCEN received approximately 4.6 million SARs and 20.8 million CTRs in FY2023, with depository institutions responsible for the majority.

The BSA/AML Officer role is federally required under 31 CFR 1020.210. It's also one of the highest-liability positions in any compliance department — as TD Bank's $1.3 billion penalty demonstrated in October 2024.

PCI DSS and 23 NYCRR 500

PCI DSS v4.0 became fully mandatory on March 31, 2025 for all entities that store, process, or transmit payment card data. 23 NYCRR 500, New York's cybersecurity regulation, was amended in November 2023 with enhanced requirements for larger entities, including 72-hour incident reporting, mandatory penetration testing, and CISO designation. NYDFS recently secured a $2.25 million cybersecurity settlement against Delta Dental for violations — a signal that enforcement of these technical standards is accelerating.

Both regulations require compliance professionals who can translate technical cybersecurity standards into regulatory language — a combination that's genuinely difficult to find in the candidate market.

Consumer Protection and Fair Lending

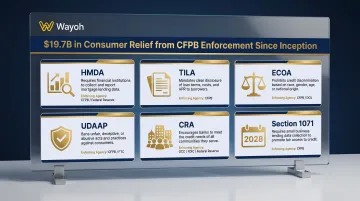

Beyond cybersecurity, lending-side regulations carry their own compliance weight. HMDA, TILA, ECOA, UDAAP, and the Community Reinvestment Act collectively require data collection, standardized disclosures, equitable treatment standards, and periodic performance examinations. CFPB enforcement since inception has produced approximately $19.7 billion in consumer relief and $5 billion in civil money penalties.

The CFPB's revised Section 1071 rule — finalizing small business lending data collection requirements with a January 1, 2028 compliance date — is broadening fair lending obligations considerably. Institutions will need compliance specialists with statistical literacy and deep familiarity with CFPB-supervised lending regulations.

State Privacy Laws

CCPA creates obligations that reach beyond federal GLBA coverage. GLBA-covered data is exempt — but marketing data, website analytics, and employee records all fall under CCPA's full requirements, including consumer access, deletion, and opt-out rights. As more states advance similar frameworks, multi-jurisdictional privacy management is becoming a distinct compliance function in its own right.

The Biggest Compliance Challenges Institutions Face Right Now

Regulatory Fragmentation

Federal agencies are recalibrating priorities while states advance independent consumer protection and privacy agendas. The result is an inconsistent compliance environment where overlapping and sometimes conflicting requirements create significant interpretation risk.

According to CSBS research, community banks bear a disproportionately high compliance cost burden relative to larger institutions — a gap that demands proactive leadership, not reactive monitoring.

Talent Shortages

83% of financial executives report experiencing a talent shortage, up from 70% in 2022. In compliance specifically, the pressure is dual-sided: senior professionals are retiring faster than replacements arrive, mid-level staff are burning out, and specialized roles sit open for months. Every day a BSA/AML Officer seat is vacant carries direct regulatory exposure. The BLS's projected 33,300 annual compliance officer openings are driven almost entirely by replacement demand — the pipeline isn't growing fast enough to cover attrition.

Fraud Escalation

The Federal Reserve's 2024 Risk Officer Survey documented significant fraud growth across multiple channels:

- Check fraud attempts up 10%; 94% of institutions experienced counterfeit checks

- ACH fraud attempts up 9%

- Debit card fraud up 6%

- Mule account activity jumped 12%

Nearly 60% of banks, fintechs, and credit unions lost over $500K in direct fraud losses in 2023. Institutions need BSA/AML leaders who build continuously improving detection frameworks — not officers maintaining static programs.

Emerging Technology Gaps

AI adoption, digital asset programs, and fintech partnerships are introducing compliance exposures that many traditional compliance officers aren't equipped to navigate. The regulatory response is already taking shape: the FDIC, Federal Reserve, and OCC issued a joint statement in July 2025 on risk-management requirements for crypto-asset safekeeping, while the Federal Reserve has separately begun setting AI supervisory expectations for financial institutions.

The demand for compliance professionals with crypto, blockchain analytics, and digital asset regulatory experience has grown sharply as a result — particularly among fintech clients building out these programs for the first time.

Compliance Roles in Financial Institutions: Who Does What

Chief Compliance Officer (CCO)

The CCO sets compliance management strategy, owns the institution's regulatory relationships, and reports to the board. This isn't a technical role — it's an executive one. Board-level communication, examiner relationship management, and the ability to navigate enforcement matters are the primary differentiators between a good CCO and a great one. Regulatory knowledge is the baseline. What actually moves the needle in a CCO search is whether the candidate can lead under regulatory pressure and maintain credibility with both the board and examiners.

BSA/AML Officer

Federally required under 31 CFR 1020.210, the BSA/AML Officer manages the AML program, suspicious activity monitoring, FinCEN reporting, and OFAC screening. Given the volume — 4.6 million SARs filed industry-wide in FY2023 — and the penalty exposure (TD Bank's $1.3 billion settlement), this is a board-level hiring priority.

Strong candidates bring:

- Deep working knowledge of BSA/FinCEN regulatory requirements

- Operational management experience across AML and OFAC programs

- Judgment to escalate the right issues at the right time

Compliance Manager or Director

This role sits between the CCO and front-line compliance staff, managing daily program operations, policy updates, training delivery, and monitoring activities. Where a CCO sets the direction, the Compliance Manager makes sure it actually gets executed. In many community banks, this person effectively functions as the de facto CCO.

Fair Lending and CRA Compliance Specialist

With CFPB's revised Section 1071 rule taking effect and HMDA reporting requirements growing more granular, this role demands statistical literacy alongside regulatory expertise. Specialists in this area need to run fair lending risk assessments, manage HMDA data integrity, and understand CRA examination methodology. CFPB scrutiny on small business lending data is expanding — institutions without dedicated fair lending expertise face growing examination risk.

Compliance Analyst

Entry-to-mid-level analysts handle testing, monitoring, documentation, and audit support — and are often the first hire when an institution starts scaling its compliance function. Building compliance pipeline here matters: the talent shortage is partly structural, and institutions that develop analysts internally are better positioned than those competing for experienced hires at every level.

What to Look for When Hiring a Compliance Leader

Define Generalist vs. Specialist First

Hiring the wrong profile is expensive. A CCO-level generalist with broad regulatory knowledge is the right hire when you need enterprise-level oversight and board engagement. A BSA/AML Officer specialist is the right hire when your AML program needs rebuilding or your examination history shows monitoring gaps. Before opening a search, define the scope: what regulatory obligations is this person primarily responsible for?

Wayoh's process starts here: helping clients shape the role before going to market, which consistently shortens time-to-hire and reduces mismatches.

Credentials That Signal Expertise

| Credential | Administering Body | Best Suited For |

|---|---|---|

| CRCM | American Bankers Association | Banking compliance generalists — consumer lending, deposit, privacy |

| CAMS | ACAMS | BSA/AML and financial crime specialists |

| CCEP | SCCE/HCCA | Broader corporate compliance and ethics leadership |

More than 65,000 professionals hold CAMS certification globally. The CRCM is specifically scoped to U.S. banking law, making it the most relevant credential for bank-side compliance generalists. Neither replaces hands-on experience, but both signal that a candidate has invested in formal, structured regulatory knowledge.

Regulatory Examination Experience

Candidates who have managed OCC, FDIC, CFPB, or state regulator examinations hit the ground running. In interviews, ask directly:

- What was their role in the most recent examination cycle?

- Have they managed findings remediation after an exam?

- Have they navigated an enforcement action or consent order?

The answers reveal whether a candidate can perform under examiner pressure — or only in steady-state conditions.

Leadership and Communication

Compliance leaders must translate complex regulatory requirements into risk language that boards and executive teams can act on. They also need to influence compliance culture across business lines that often treat compliance as an obstacle rather than a function.

During interviews, assess this directly: ask how they've handled conflicts between business unit growth goals and compliance requirements. Strong technical knowledge paired with weak leadership tends to produce departments that pass examinations but fail to drive real compliance behavior across the organization.

How to Hire Compliance Leaders in a Competitive Market

With $4.3 billion in 2024 penalties, record enforcement intensity across SEC, FinCEN, and CFPB, and only 3% projected employment growth in compliance, the supply-demand imbalance for experienced talent is structural — not cyclical.

Build Your Employer Value Proposition First

Top compliance candidates evaluate:

- How leadership positions compliance — strategic function or cost center

- Board and C-suite investment in headcount, technology, and training

- Examination history and institutional stability

- Clarity on scope, authority, and reporting structure for the role

Develop a clear, honest narrative around these factors before going to market. Candidates with options will ask directly, and vague answers read as warning signs.

Use Structured, Scenario-Based Interviews

Credentials alone don't predict performance. Build interview questions around real regulatory situations: How would you handle a product launch that creates UDAAP exposure? What does your BSA program look like six months after you join? Involve current compliance leadership in evaluation — they'll ask questions HR can't.

Partner with a Recruiter Who Specializes in Compliance

The strongest compliance candidates aren't browsing job boards. They're known quantities within specialist networks — professionals who receive direct outreach before they're actively looking.

Wayoh has spent over 3 years placing compliance, risk, and legal professionals across banking, fintech, and healthtech — with 500+ placements in regulated industries. Built on a human-first recruiting approach, the firm maintains direct relationships with active and passive candidates across roles like BSA/AML Officers, CCOs, and fair lending specialists. For senior searches, that network access consistently shortens time-to-fill in a market where qualified candidates are rarely available and highly sought.

Wayoh also offers interim compliance staffing for institutions that need immediate coverage while a permanent search runs in parallel. Every interim consultant is fully vetted with references and background checks before placement — especially important in roles where regulatory awareness and confidentiality are non-negotiable.

Frequently Asked Questions

What is financial regulatory compliance?

Financial regulatory compliance is the set of laws, standards, and practices financial institutions must follow to operate legally and ethically. It's governed by federal agencies — the OCC, FDIC, CFPB, SEC, and FINRA — alongside state regulators whose requirements frequently overlap.

What are compliance roles in finance?

The primary compliance roles are Chief Compliance Officer, BSA/AML Officer, Compliance Manager, Fair Lending Specialist, and Compliance Analyst. Each role covers a distinct area of a financial institution's regulatory obligations, spanning enterprise strategy down to transaction-level monitoring.

How do banks ensure compliance with regulatory requirements?

Banks maintain compliance through written policies, employee training, internal audits, regulatory monitoring programs, and a qualified compliance team. Examination preparation and findings remediation are continuous responsibilities layered on top.

What regulatory challenges do financial institutions face today?

Institutions face overlapping federal and state regulations, talent shortages across compliance functions, escalating fraud losses, and emerging technology exposures — particularly around AI and digital assets — that traditional compliance frameworks were not designed to handle.

What are the four stages of compliance?

The four stages are: identification (understanding which regulations apply), implementation (building policies and controls), monitoring (ongoing testing and audits), and remediation (addressing findings and gaps). Most institutions run all four stages at once, each applied to different regulatory areas.

What are the five key areas of compliance in financial services?

The five core areas are consumer protection, anti-money laundering (BSA/AML), data security and privacy, operational compliance, and lending compliance. Managing all five at once is the baseline expectation — dedicated specialists are typically needed across several of them.