This article is for HR leaders, compliance heads, and C-suite executives at banks, fintechs, and financial institutions. AI is now embedded in credit decisioning, fraud detection, and automated trading — and the accountability obligations that come with it are no longer optional. Regulators are watching, boards are asking questions, and the gap between how AI systems behave and how firms can explain that behavior is growing.

What follows covers how the hiring process works, which roles are in scope, what skills to evaluate, and where firms most commonly go wrong.

Key Takeaways

- These roles require cross-disciplinary profiles spanning regulation, data science, risk, and ethics — not a compliance-only hire

- Regulatory pressure from the OCC, CFPB, and Federal Reserve makes governance roles operationally necessary, not optional

- Define the role archetype, reporting structure, and applicable frameworks before sourcing begins

- Common mistakes: treating this as a senior compliance hire or prioritizing credentials over cross-disciplinary performance

- Firms with limited AI deployments may be better served distributing governance responsibilities rather than creating a standalone role

What Is the Hiring Process for AI Ethics and Governance Professionals?

Hiring AI ethics and governance professionals is a specialized talent acquisition process — one focused on finding candidates who can govern how AI systems are built, deployed, audited, and corrected inside a regulated financial environment. The roles in scope range from Chief AI Ethics Officer to Model Risk Officer to Responsible AI Program Lead, each requiring a different blend of technical, legal, and operational competency.

How It Differs from Compliance or Technology Hiring

Most firms struggle to categorize this hire accurately, and that's where searches go wrong. The role spans compliance, technology, and policy — and purely functional hiring processes are not built for that:

- Unlike compliance hiring: candidates need fluency in model behavior, data pipelines, and quantitative bias metrics, not just rule sets

- Unlike engineering hiring: candidates must understand fair lending law, model risk management frameworks, and how to brief a board or regulator

- Unlike policy hiring: the role requires operational execution, not just document production

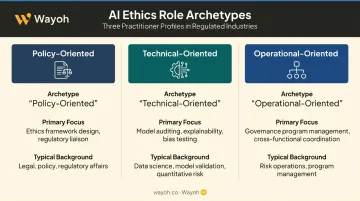

Three Core Role Archetypes

Before any search begins, firms need clarity on which archetype they need:

| Archetype | Primary Focus | Typical Background |

|---|---|---|

| Policy-Oriented | Ethics framework design, regulatory liaison | Legal, policy, regulatory affairs |

| Technical-Oriented | Model auditing, explainability, bias testing | Data science, model validation, quantitative risk |

| Operational-Oriented | Governance program management, cross-functional coordination | Risk operations, program management, compliance operations |

Hiring for the wrong archetype is one of the most common causes of a failed search. It typically traces back to a job description written before anyone agreed on what the role was actually meant to solve.

Why Financial Services Companies Need These Professionals Now

Regulatory pressure is the most immediate driver. The OCC, CFPB, Federal Reserve, and FDIC have all issued guidance relevant to AI governance in financial services. SR 11-7, the Federal Reserve's model risk management framework, sets expectations for how models are validated, monitored, and challenged — and AI systems fall squarely within its scope.

The CFPB has been particularly active. CFPB Circular 2022-03 confirmed that lenders using complex algorithms for credit decisions must still provide specific, accurate adverse action reasons — a direct governance challenge for firms using black-box models. The Bureau reinforced this in subsequent guidance, explicitly stating that automated systems do not excuse compliance with existing law.

For institutions operating across borders, the EU AI Act adds another layer: it classifies most financial AI systems as high-risk, triggering documentation, transparency, and human oversight requirements that mirror what U.S. regulators are already signaling domestically.

Operational Risks Without Dedicated Oversight

Without a named governance function, firms accumulate specific, measurable risks:

- Algorithmic bias in lending decisions that cannot be defended in an examination

- Credit denials that lack the explainability required under Regulation B and ECOA

- Fraud detection models that disproportionately flag certain demographic groups

- Automated trading behavior that generates conduct risk during volatility events

The Apple Card/Goldman Sachs algorithm investigation in 2019 illustrated the reputational and regulatory exposure that follows when AI credit decisions appear to produce gender-disparate outcomes — even without confirmed violations, the scrutiny was costly.

The Gap Between Compliance and Data Science

Most compliance teams cannot interrogate model behavior at a technical level. Most data science teams do not know what constitutes a discriminatory outcome under ECOA or Regulation B. The people who understand the models and the people who understand the rules rarely sit in the same room. That disconnect is where governance failures build — quietly, until an examiner or regulator surfaces them. A dedicated AI ethics professional bridges both sides: someone who can read a model card and a compliance brief, and translate between them.

How the Process Works: From Role Definition to Final Selection

The end-to-end process follows a defined sequence: role scoping and stakeholder alignment → skills profile and job architecture → sourcing from a narrow, often passive talent pool → multi-stage assessment → offer and integration planning.

Step 1: Role Architecture and Internal Alignment

Before the search begins, the hiring team must determine:

- Which archetype is needed (policy, technical, or operational)

- Which regulatory frameworks the role will be accountable to (SR 11-7, ECOA, CFPB guidance, EU AI Act)

- Who the role reports to — legal, risk, technology, or the C-suite

- What governance infrastructure already exists and what needs to be built

Misalignment on these questions before sourcing starts is the single most common cause of a failed search. Wayoh's intake process for senior governance and compliance searches begins with exactly these questions — reporting structure, mandate clarity, and organizational context — before any candidate outreach begins.

Step 2: Candidate Sourcing and Market Mapping

This is where the process becomes genuinely difficult. The candidate pool is small, passive, and highly sought-after. Professionals with the right combination of AI technical literacy, financial regulatory knowledge, and applied ethics reasoning are not browsing job boards.

Useful sourcing channels include:

- Model risk teams at large banks and regional institutions

- Financial regulatory bodies (OCC, CFPB, Federal Reserve examiners moving to the private sector)

- Academic AI ethics and responsible AI programs

- Specialist fintech governance and risk operations teams

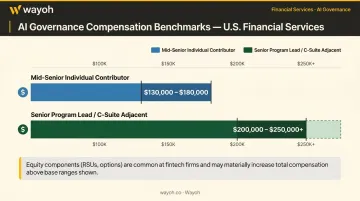

Compensation for AI governance and responsible AI roles in U.S. financial services ranges from approximately $130,000–$180,000 for mid-senior individual contributors, with senior program leads and C-suite adjacent positions reaching $200,000–$250,000 or higher at major institutions. Fintech firms often layer in equity components on top.

Firms that cannot benchmark accurately will lose candidates before the offer stage.

Specialist recruiters with compliance and risk networks — like Wayoh, whose human-first recruiting approach prioritizes relationship-based access over keyword searching — are frequently engaged at this stage precisely because the passive candidate market demands that level of personal engagement.

Step 3: Assessment and Selection

A strong assessment framework tests four dimensions, not two:

- Regulatory knowledge — model risk management (SR 11-7), fair lending, ECOA, CFPB adverse action requirements

- Technical comprehension — ability to evaluate model outputs, identify bias vectors, interpret feature importance

- Scenario-based judgment — "A regulator has requested explainability documentation for your mortgage underwriting model within 30 days. Walk us through your response."

- Stakeholder communication — presenting governance findings to a board, briefing legal counsel on a model audit result

The panel should include representatives from risk, legal, and technology leadership — not just HR. Scoring rubrics applied consistently across candidates prevent the assessment from drifting based on interviewer preference.

Key Factors That Affect This Process in Financial Services

- Regulatory environment and firm type: hiring criteria for a nationally chartered bank governed by OCC and SR 11-7 differ from those at a state-supervised fintech startup — the applicable framework must shape the job architecture from day one

- Scarcity of cross-disciplinary candidates: firms that cannot articulate why their opportunity is compelling will lose candidates to larger institutions with stronger brands or higher budgets; the pitch matters

- Organizational maturity of AI governance: a firm with existing model risk infrastructure needs a leader who can extend it; a firm starting from scratch needs a builder. These are different profiles, and sourcing each one effectively requires a different approach.

- Reporting structure and decision-making authority: experienced candidates will probe whether the role has real authority or is a compliance checkbox; roles that report into technology rather than risk or legal often face skepticism from the strongest candidates

- Process discipline and speed: this is a thin market where top candidates evaluate multiple offers simultaneously — disorganized, multi-month processes consistently lose to structured ones; specialist recruiters like Wayoh shorten time-to-shortlist by working from established networks rather than starting searches from scratch

Common Hiring Mistakes and Misconceptions

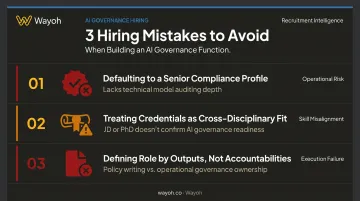

Several patterns consistently derail these searches. Here are the three that surface most often.

Defaulting to a senior compliance profile. Candidates from traditional compliance backgrounds often lack the technical depth to audit model behavior, interpret feature importance, or assess fairness metrics. The role demands genuine AI literacy — not just regulatory familiarity.

Treating credentials as a proxy for cross-disciplinary fit. A JD, PhD, or CISO title doesn't confirm readiness for this role. Someone who wrote AI ethics policy at a tech company may have no working knowledge of fair lending law, model validation standards, or bank examiner interactions.

Defining the role by its outputs, not its accountabilities. Organizations that frame success as "producing an AI ethics policy" end up hiring a policy writer when they need an operational governance lead — or vice versa. Get specific about what this person owns in the model lifecycle, not just what documents they'll produce.

When a Dedicated AI Ethics Hire May Not Be the Right Move

Not every firm needs a standalone hire. The following situations suggest the organization is not ready:

- Fewer than three AI models in production with limited regulatory scrutiny of those deployments

- No formal model risk function and no documented AI review process

- No board-level mandate for algorithmic accountability

In these cases, distributing governance responsibilities across existing compliance, data science, and legal staff — with a defined RACI and clear ownership — is a better fit than creating a full-time role that will lack sufficient operational scope.

That structural fix only works if leadership is aligned on what governance actually requires. When executives expect one hire to absorb all AI accountability — without policy infrastructure, cross-functional training, or board-level commitment — the role is likely to fail regardless of how strong the candidate is. The hire should follow governance intent, not substitute for it.

Frequently Asked Questions

What qualifications should an AI ethics and governance professional have in financial services?

The strongest candidates combine technical AI literacy (model auditing, bias testing, explainability methods) with regulatory knowledge of fair lending, ECOA, and SR 11-7, plus demonstrated experience translating ethical principles into operational protocols. All three dimensions need to be present — not just one or two.

How is an AI ethics and governance role different from a compliance officer role?

Compliance officers manage adherence to existing rules. AI ethics and governance professionals proactively design the frameworks, review protocols, and audit mechanisms that determine how AI systems are built and overseen — a function that requires technical depth most compliance teams do not hold.

When should a financial services company hire a dedicated AI ethics professional?

Hire when you have multiple AI models in production, active regulatory scrutiny of algorithmic decision-making, board-level concern about reputational risk, or no documented governance process that could withstand an examiner inquiry.

What does a typical interview process look like for an AI ethics candidate?

A structured multi-stage process should include a regulatory knowledge assessment, a model review case study, and a stakeholder communication exercise. The evaluation panel should include risk, legal, and technology leadership — not just HR.

Which U.S. regulators require or recommend AI ethics oversight in financial services?

The OCC, CFPB, Federal Reserve, and FDIC are the primary bodies. SR 11-7 on model risk management and CFPB guidance on algorithmic fairness and adverse action are the most commonly cited frameworks driving the need for dedicated governance roles.

What salary range should financial services firms budget for an AI ethics and governance professional?

Mid-senior roles in U.S. financial services typically range from $130,000 to $180,000. Senior program leads and C-suite adjacent positions at major banks or well-funded fintechs can reach $200,000 to $250,000 or above, with equity components common at growth-stage firms.