The problem: qualified ML model governance experts are exceptionally rare. The role sits at the crossroads of data science, financial regulation, and model risk management — a combination that few professionals have genuinely mastered. Most ML engineers lack SR 11-7 fluency. Most compliance officers can't interrogate a gradient boosting model's training data. Banks end up with governance programs that look good on paper but fall apart under examination.

This article covers what ML model governance means for financial institutions, what strong candidates actually look like, why this hiring market is so difficult, and how Wayoh helps banks and fintechs secure this talent before their next examination cycle.

Key Takeaways

- ML model governance is a regulated control function — not a data science add-on — requiring documentation, independent validation, monitoring, and board-level reporting

- Governing frameworks include SR 11-7, the updated SR 26-2 / OCC Bulletin 2026-13 (April 2026), and EU AI Act obligations for institutions with European exposure

- Strong candidates combine quantitative depth with hands-on regulatory experience — most have one, rarely both

- Compensation for senior model risk roles in New York runs $250,000–$450,000 base, creating fierce competition with hedge funds and fintechs

- Wayoh's relationship-led sourcing reaches governance professionals who aren't actively posting resumes

What ML Model Governance Means for Financial Institutions

ML model governance is the end-to-end framework of controls, processes, and documentation that manages how machine learning models are developed, validated, approved, deployed, monitored, and retired — with the goal of ensuring models perform as intended and remain compliant with regulatory and business requirements.

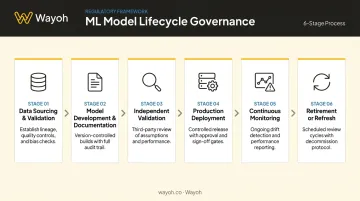

The Model Lifecycle That Needs Governing

For U.S. banks, the lifecycle stages requiring oversight are:

- Data sourcing and validation — lineage tracking, quality controls, bias checks on training data

- Model development and documentation — clear records of methodology, assumptions, and intended use

- Independent model validation — back-testing, sensitivity analysis, benchmarking against challenger models

- Production deployment — version control, approval workflows, change management

- Continuous monitoring — drift detection, performance degradation alerts, demographic fairness checks

- Model retirement or refresh — governance documentation when models are decommissioned or replaced

The Regulatory Foundation

The core U.S. framework is SR 11-7, which defines a model as "a quantitative method, system, or approach using statistical, economic, financial, or mathematical theories, techniques, and assumptions to process input data into quantitative estimates." It requires a firm-wide model inventory, independent validation, governance policies, documentation, and board/senior management reporting.

Beyond SR 11-7, institutions operating across multiple jurisdictions face additional layers of obligation:

| Framework | Scope | Key Requirement |

|---|---|---|

| SR 11-7 | U.S. bank holding companies | Firm-wide model inventory, independent validation, board reporting |

| BCBS 239 | Internationally active banks | Risk data aggregation and reporting across key internal models |

| EU AI Act | Institutions with EU exposure | High-risk classification for creditworthiness scoring and insurance risk models |

The stakes are concrete: these models directly affect credit approvals, loan pricing, fraud flags, and AML alerts. Regulatory errors translate into enforcement actions, consumer protection violations, and balance sheet losses — which is why governance roles in financial services carry a different weight than in most other industries, and why finding the right talent requires more than a keyword search.

Why Financial Institutions Are Racing to Hire Governance Experts

Regulatory Pressure Has Real Teeth

Model governance failures have produced documented OCC enforcement actions. In 2023, United Fidelity Bank received a consent order requiring it to identify the full population of key internal models, address model validation deficiencies, and perform risk-based validation. In 2024, City National Bank faced remediation requirements for independent validation of BSA/AML monitoring models and filtering thresholds.

These are exam findings with lasting consequences: mandatory remediation, reputational damage, and heightened scrutiny that follows institutions into future exam cycles.

Expanding Model Inventories

The scope of what needs governance has grown sharply. Banks now run ML models across:

- Credit underwriting and adverse-action determination

- Real-time fraud detection

- Customer segmentation and marketing targeting

- AML transaction monitoring

- Stress testing and capital planning

Deloitte's EMEA model risk survey found large banks average approximately 650 models in their inventories — each requiring documented governance, validation, and monitoring. That's not a monitoring problem; it's a structural staffing problem.

Compounding Framework Obligations

Beyond SR 11-7, institutions face widening scope from multiple directions:

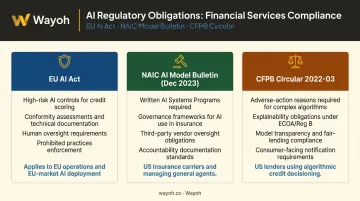

- EU AI Act requires high-risk AI controls for credit scoring systems at firms with European operations

- NAIC AI Model Bulletin (adopted December 4, 2023) expects insurers to maintain written AI Systems Programs covering governance, risk management, validation, and third-party oversight

- CFPB Circular 2022-03 makes clear that ECOA/Regulation B require specific adverse-action reasons even when complex algorithms are used — black-box complexity is not a defense

Beyond Compliance: Business Continuity Risk

The regulatory exposure is only part of the picture. Ungoverned models carry operational risks that affect performance directly:

- Model drift degrades credit portfolio performance before anyone notices

- Biased outputs expose institutions to fair lending litigation

- AML false positives at scale overwhelm compliance operations

Institutions that treat model governance as a staffing priority — rather than a remediation task — avoid these cascading failures before they reach examiners.

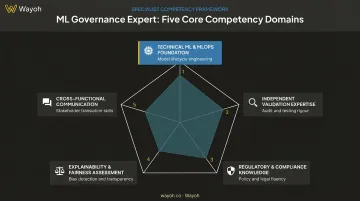

The Skills That Define a Strong ML Governance Expert

Most candidates have depth in one domain. Strong governance hires have genuine competence in all five.

Technical ML and MLOps Foundation

Governance professionals don't need to actively build models — but they must be able to interrogate them. This means familiarity with:

- Model registries, versioning, and CI/CD deployment pipelines

- Training data composition and data lineage documentation

- Performance metrics and their limitations (accuracy vs. AUC vs. calibration)

- Monitoring tooling for drift detection and data quality alerts

Independent Validation Expertise

Under SR 26-2 guidance, independent validation is a required control function — not an optional quality check. Strong validators can:

- Execute back-testing, sensitivity analysis, and benchmarking against challenger models

- Detect overfitting and identify out-of-sample performance degradation

- Produce or critique a Model Validation Report (MVR) that satisfies current MRM guidance

- Maintain sufficient independence from model development and use

Regulatory and Compliance Knowledge

Candidates must understand SR 11-7/SR 26-2 as a working control framework, not just a regulatory reference. Strong hires demonstrate practical knowledge across:

- Model risk appetite frameworks and how SR 11-7/SR 26-2 governs internal audit requirements

- OCC interpretive guidance on model risk management

- GDPR Article 22 automated-decision rights for cross-border institutions

- NAIC AI governance expectations for any insurance-adjacent use cases

Explainability and Fairness Assessment

CFPB Circular 2022-03 established that creditors must provide specific adverse-action reasons regardless of model complexity. Governance specialists need to:

- Apply explainability methods (SHAP, LIME) to document feature importance

- Map model outputs to adverse-action reason codes for consumer-facing decisions

- Assess demographic disparities and document fair lending analysis

- Translate findings into audit-ready documentation under ECOA and FCRA

Cross-Functional Communication

This is the skill most screened for too lightly. Governance professionals must translate complex model behavior into governance committee presentations, regulatory examination responses, and written model risk reports that auditors and examiners can act on. Without that communication layer, even technically sound governance work won't hold up under OCC examination.

Why Hiring ML Governance Talent Is So Difficult

The Dual-Expertise Problem

People who know ML well usually don't know SR 26-2. People who know SR 26-2 usually can't interrogate a model's architecture. Accepting a candidate who is strong in one domain but weak in the other produces a governance program that looks credible internally but fails under independent examination.

According to Selby Jennings' 2024/25 U.S. Risk Management Compensation Guide, Managing Director-level Model Risk/Analytics roles in New York command $250,000–$450,000 base and $600,000–$1.2M total compensation. That's far above what BLS reports as the mean for Financial Risk Specialists broadly ($116,140).

Competitive Pressure from Outside Banking

That compensation gap becomes more painful when you factor in who else is competing for these professionals. Hedge funds, AI-native fintechs, and large technology firms recruit the same candidates — often at compensation levels regional and community banks cannot match. The already-small pool of dual-domain experts shrinks further when competing against firms unconstrained by standard HR compensation bands.

Internal Screening Limitations

Narrowing the candidate pool is only part of the problem. Most talent acquisition teams also lack the domain knowledge to assess whether a candidate's model validation experience is SR 26-2-grade or too generalist to satisfy examiners. A resume listing "model validation" could mean regulatory-grade independent challenge or a brief quality check on a business analytics tool. That distinction is critical during examination — and it isn't visible without substantive technical and regulatory screening.

How Wayoh Places ML Governance Experts in Financial Institutions

Wayoh specializes in regulated-industry hiring across banking, fintech, and healthtech, with 500+ placements in compliance, risk, legal, and governance functions. For ML governance roles specifically, that depth changes how screening works — and who gets surfaced.

Substantive Candidate Evaluation

Wayoh's recruiters screen through direct conversation, not keyword matching. Each candidate is assessed on:

- Depth of hands-on regulatory framework experience (SR 11-7, OCC guidance)

- Validation methodology and MVR documentation history

- Ability to defend findings under regulatory examination

- Communication skills with senior stakeholders and examiners

For governance roles, the gap between a candidate who can cite SR 11-7 and one who has built and defended validation documentation under examination is significant. Wayoh's sector experience identifies that difference early.

Relationship-Led Sourcing for Passive Candidates

The strongest model risk officers, independent validators, and MLOps compliance specialists often aren't actively searching. They're placed, performing well, and not posting resumes. Rooted in a human-first recruiting philosophy, Wayoh maintains ongoing relationships with governance professionals across its banking and fintech networks. That reach enables direct outreach to candidates who would consider the right opportunity but won't appear in a job board search.

Interim Coverage for Examination Cycles

Regulatory examinations don't wait for permanent search timelines. Wayoh supports both permanent placements and interim staffing for banks that need qualified governance coverage quickly — during examination preparation, model remediation projects, or urgent inventory gaps. All interim candidates are vetted with references and background checks before placement.

Banks and fintechs in New York, California, and Florida can reach Wayoh at hiring@wayoh.com to discuss open governance roles, or candidates can contact apply@wayoh.com directly.

Frequently Asked Questions

What is machine learning model governance?

ML model governance is the structured set of policies, processes, and controls used to manage how machine learning models are developed, validated, deployed, and monitored. For financial institutions, it ensures models perform as intended, comply with regulatory requirements like SR 11-7/SR 26-2, and remain auditable throughout their lifecycle.

What is LLM governance in banking?

LLM governance applies model risk management principles to large language models, covering output monitoring, prompt auditing, bias evaluation, and explainability. No formal U.S. regulatory definition exists yet — banks govern LLMs through existing model risk, consumer compliance, and operational risk frameworks based on use case.

What qualifications should an ML model governance expert have in banking?

Strong candidates typically combine a quantitative background (statistics, data science, or applied mathematics) with hands-on SR 11-7/SR 26-2 model validation experience, risk documentation skills, and familiarity with fair lending laws. FRM designation or advanced degrees in finance or quantitative fields are common markers at regulated institutions.

Why is it hard to find ML model governance specialists?

The role requires a rare overlap of ML technical fluency and financial regulatory expertise. Most ML professionals lack compliance depth; most risk officers lack the quantitative skills to interrogate model architecture. That dual-domain gap makes this one of the harder specialist hires in regulated financial services.

What are the seven Sutras of AI governance?

The seven Sutras comes from India's AI Governance Guidelines (IndiaAI/MeitY, 2025) and covers principles like trust, accountability, fairness, explainability, and safety. It is not a U.S. banking standard, but its themes mirror what OCC and EU AI Act guidance already require of financial model governance programs.