The Federal Reserve, OCC, and FDIC updated their model risk management guidance in April 2026 through SR 26-2, while the CFPB has been explicit: complex algorithms are not an excuse for failing to comply with ECOA or adverse action notice requirements. Globally, the EU AI Act classifies credit-scoring AI as high-risk by definition.

Yet the bigger challenge facing most institutions isn't the regulatory framework. It's people. Building a functioning AI governance infrastructure requires a specific kind of professional — someone who understands model risk methodology, can read regulatory guidance, and knows how banking operations actually work. That combination is rare, and demand is growing faster than supply.

This post covers what AI governance requires in practice, the key risks banks must manage, the roles they're actively hiring for, and why sourcing this talent requires a recruiter with genuine domain knowledge.

Key Takeaways

- AI governance in banking means policies, controls, and accountable human oversight — enforced in practice, not just written on paper

- Key drivers include SR 11-7, CFPB algorithmic guidance, and the EU AI Act's high-risk classification of credit-scoring systems

- In-demand roles include model risk managers, AI compliance officers, data governance leads, and operational risk professionals with AI scope

- The talent pool is narrow, the skills are unusual, and general recruiters lack the domain knowledge to screen effectively

- Wayoh places compliance, risk, and legal professionals in regulated financial institutions — including the AI governance roles banks are building now

What AI Governance Actually Means for Banks

AI governance in banking is the combination of policies, accountability structures, and operational controls that ensure AI systems behave accurately, fairly, and in compliance with applicable law. The definition is clean. Building the actual capability is not.

SR 26-2, issued April 2026, supersedes SR 11-7 and calls for a risk-based approach tailored to each institution's model complexity and risk profile. The updated guidance explicitly excludes generative and agentic AI from its scope — a separate rulemaking process for those systems is forthcoming.

For consumer-facing AI, the CFPB has been clear: creditors cannot justify noncompliance with ECOA by claiming their algorithms are too complex to explain. Adverse action notices must provide specific reasons, regardless of model complexity. That requirement alone creates meaningful governance obligations.

Internationally, the EU AI Act — in force since August 2024 — classifies AI systems that evaluate creditworthiness or establish credit scores as high-risk. That designation carries requirements for transparency, human oversight, and bias testing.

As the EBA has noted, this framework is actively shaping how regulators globally think about AI in financial services.

The distinction that matters most for banks: compliance sets the floor. Institutions that build genuine governance capacity — dedicated roles, tested processes, documented oversight — earn measurable advantages in regulator relations and operational resilience. That gap between checking boxes and building real infrastructure is where hiring decisions make the difference.

Key AI Risks Banks Must Govern

Governance failures in AI don't happen in the abstract — they show up as regulatory findings, fair lending violations, and fraud losses. Five risk categories demand active management.

Model Risk and Drift

Machine learning models can degrade in accuracy as real-world data distributions shift over time. Unlike traditional statistical models, many ML systems are difficult to interpret, making drift detection more complex. SR 11-7 maintains enforceable supervisory expectations for model validation, documentation, and ongoing monitoring — even as the scope of what counts as a "model" continues to evolve.

Algorithmic Bias and Fair Lending

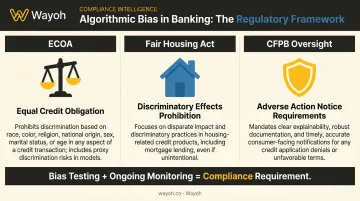

Training data that reflects historical lending patterns can produce AI outputs that discriminate against protected classes. The legal exposure is real: ECOA, the Fair Housing Act, and CFPB oversight all apply. HUD's 2024 guidance confirmed that the Fair Housing Act prohibits practices with unjustified discriminatory effects even when AI or algorithms are involved. Bias testing and ongoing monitoring are compliance requirements, not discretionary controls.

Data Privacy and PII Misuse

AI systems in banking ingest large volumes of personally identifiable information. The CFPB's 2023 chatbot report identified specific risks: privacy exposure in chat logs, disclosure risk when LLM training data contains personal information, and breach exposure from AI-generated interactions.

GLBA obligations apply throughout. Governance must include data lineage documentation and access controls from the point of system design, not as an afterthought.

Adversarial and Cybersecurity Risk

FSOC's 2025 Annual Report identifies data poisoning as an AI-specific cybersecurity risk. Treasury's 2024 AI report flagged generative AI's capacity to enable deepfakes, synthetic identities, and more convincing phishing — risks that directly affect customer identification and fraud detection systems. Existing IT controls aren't sufficient; AI systems need security governance layers designed for their specific vulnerabilities.

Accountability Gaps and Explainability Failures

When an AI system denies a loan or flags a transaction as suspicious, a designated owner within the institution must be accountable and able to explain the outcome to a regulator or customer. Governance frameworks need to define who owns AI decisions and ensure systems can produce human-interpretable rationale. Institutions that lack this structure face examiner findings they're not positioned to defend.

Why Building an AI Governance Team Is Harder Than It Looks

Most banks understand what governance requires. The harder problem is staffing it.

The Skills Overlap Problem

Professionals who can govern AI in a regulated bank must combine:

- Financial regulation knowledge (SR 26-2, ECOA, GLBA, OCC guidance)

- Model risk methodology (validation, documentation, ongoing monitoring)

- Data science literacy (enough to assess model outputs and challenge developers)

- Internal audit and control design experience

That combination doesn't come from a single academic program or career path. Hiring managers often lack a clear profile for what "good" looks like — which means poorly scoped job descriptions and wasted time on candidates who check one or two boxes but not all four.

Deployment Is Outpacing Oversight

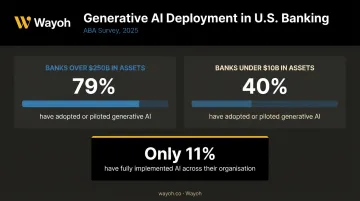

An ABA survey published in 2025 found that 43% of financial institutions were actively deploying generative AI, and 42% had created dedicated groups to oversee it. But only 11% had fully implemented it — meaning oversight functions are being built while systems are already running. That sequence creates exposure.

The same survey found 79% of banks over $250 billion in assets had generative AI live or in the pipeline, compared to 40% of banks under $10 billion. Governance capacity is not scaling at the same rate.

Upskilling Has Limits

Many banks attempt to retrain existing compliance or risk staff for AI governance roles. The challenge: AI governance requires comfort with probabilistic reasoning, ML model outputs, and evolving regulatory interpretation that takes time to build.

A 2024 Arizent survey reported that 26% of banking professionals couldn't distinguish between traditional AI and generative AI — a meaningful gap when those same professionals are expected to govern the systems.

Deloitte's research on agentic AI in financial services identifies emerging roles — AI risk officers, behavior auditors, simulation specialists — that have no direct equivalent in current job families. These aren't roles you fill by reassigning a compliance analyst.

Geographic Concentration

The deepest candidate pools for AI risk talent sit in a handful of markets:

- New York and San Francisco lead in both volume and seniority of available candidates

- Secondary markets like Chicago, Charlotte, and Boston have growing but thinner pipelines

- Banks outside these geographies often lack the recruiter relationships to access passive candidates — the majority of this talent pool

For institutions not headquartered in major financial centers, that access gap is often the core hiring problem.

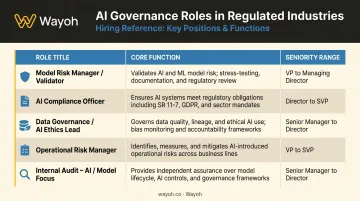

The AI Governance Roles Banks Are Actively Recruiting For

Banks are staffing these functions now — and while structure varies by institution size, the core hiring categories hold steady across community banks, regionals, and large nationals.

| Role | Core Function | Seniority Range |

|---|---|---|

| Model Risk Manager / Validator | Validates AI/ML models for accuracy, stability, and SR 26-2 compliance | Analyst to Head of Model Validation |

| AI Compliance Officer | Translates OCC, CFPB, and Fed guidance into internal policy and controls | Manager to VP |

| Data Governance / AI Ethics Lead | Manages training data quality, bias audits, explainability standards | Lead to Director |

| Operational Risk Manager (AI scope) | Designs control testing programs for AI systems, including monitoring and escalation | Manager to SVP |

| Internal Audit (AI/Model focus) | Audits AI model governance, control effectiveness, and documentation completeness | Senior Auditor to Audit Director |

A few notes on each:

Model risk validators with ML experience (not just traditional statistical models) are in genuinely short supply. The original SR 11-7 validation methodology was designed for econometric models — applying it to gradient-boosted classifiers or neural networks requires a different kind of expertise.

AI compliance officers need to hold two bodies of knowledge simultaneously: model risk governance and consumer protection law. Most candidates are strong in one — finding someone fluent in both is a recurring challenge for hiring teams.

Data governance leads now sit squarely in exam scope. CFPB scrutiny on algorithmic decisions and the EU AI Act's bias documentation requirements have turned training data governance from a best practice into a line item regulators check.

RIMS reported that the median base salary for U.S. risk management professionals reached $160,000 in 2025, up from $144,000 in 2023 — a broad benchmark that reflects the competitive pressure across the entire risk function.

How Wayoh Helps Banks Hire Specialized AI Risk and Governance Talent

The Limitation of General Recruiting

Most staffing firms approach compliance and risk hiring the way they approach any other search — keyword matching, resume screening, volume pipelines. That works for well-defined roles where the requirements are clear and the candidate pool is large.

AI governance roles are neither. A recruiter who can't assess whether a candidate understands SR 26-2 validation methodology or can explain the difference between model drift and algorithmic bias will pass along pipelines that waste hiring managers' time. For banks under regulatory pressure to build governance capacity quickly, that's a real operational risk — not just a slow search.

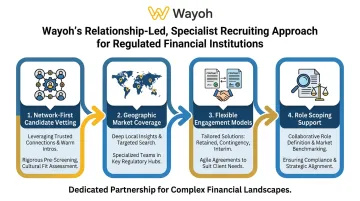

Wayoh's Approach

Wayoh is a human-first, relationship-led recruiting firm built specifically for compliance, risk, and legal hiring in regulated financial institutions. With over 500 placements across community, commercial, and investment banks, the team brings working knowledge of model risk functions, regulatory expectations, and how governance roles actually operate inside a bank.

What that looks like in practice:

- Pre-vetted candidates: Wayoh's network-first model means candidates are assessed through direct conversations, not just resume review. The team evaluates technical fit, regulatory knowledge, and banking operations experience before a profile reaches a hiring manager.

- Active networks in key markets: Wayoh recruits across New York, California, Florida, and other major U.S. financial centers — the geographies where AI governance talent concentrates.

- Flexible engagement models: Wayoh supports permanent hires, interim placements for project-based governance buildouts, and multi-position searches for banks constructing governance functions from the ground up.

- Role scoping support: For emerging positions where hiring managers don't yet have a clear internal benchmark, Wayoh works consultatively to define the role, calibrate seniority, and map the candidate market.

To discuss a current search or explore how Wayoh can support your AI governance hiring, reach out at hiring@wayoh.com.

Frequently Asked Questions

How is AI used in the banking industry?

Banks deploy AI across fraud detection, credit underwriting, AML transaction monitoring, customer service automation, KYC/identity verification, and back-office process automation. The Treasury's 2024 AI report identifies these as primary use cases, with governance complexity varying significantly by application and risk level.

What is an example of AI governance in banking?

A bank deploying an AI credit scoring model establishes governance through a structured end-to-end process:

- Pre-deployment model validation against SR 26-2 expectations

- Bias testing against protected class outcomes

- Explainability documentation for adverse action notices

- Performance monitoring thresholds that trigger automatic revalidation

What roles do banks typically hire for AI governance?

The most common roles are model risk validators, AI compliance officers, data governance leads, operational risk managers with AI scope, and internal auditors focused on model and AI risk. Seniority ranges from analyst to senior leadership, with some larger institutions now establishing Chief AI Officer positions.

Why is hiring specialized AI risk talent so difficult for financial institutions?

These roles demand quantitative literacy, regulatory fluency, and hands-on banking operations experience — a combination that narrows the candidate pool significantly. Most general recruiters lack the domain knowledge to screen accurately, which produces weak pipelines and extended search timelines.

What regulations are driving AI governance requirements in U.S. banks?

The primary drivers are SR 26-2 (updated model risk management guidance), OCC Bulletin 2026-13, CFPB Circular 2022-03 on algorithmic adverse action notices, and the five-agency 2021 AI RFI framework. The EU AI Act's high-risk classification of credit-scoring AI is also influencing how U.S. regulators approach the category.

How does a specialized recruiter help with AI governance hiring?

Specialized recruiters bring established networks of vetted professionals, the domain knowledge to screen for genuine AI governance competency rather than keyword matches, and the ability to move quickly in a competitive market. That reduces time spent on unqualified candidates — which matters when governance buildout timelines are tight.