Introduction

Banking has committed to AI at scale. IDC estimated banking AI investment at $31.3 billion in 2024 — the largest of any industry globally — with fraud detection, credit underwriting, AML monitoring, and risk modeling all running on AI systems across institutions of every size.

Governance hasn't kept pace. According to an IIF-EY survey of financial services firms, only 44% had aligned a C-suite owner for AI/ML ethics and governance — while 30% were still defining who that person or team should be. Regulators, customers, and investors aren't waiting for the other 56% to catch up.

The talent gap is specific: most institutions need leaders who can bridge technical AI capability with compliance, ethics, and regulatory expertise. That profile is rare and in high demand.

This article covers what responsible AI leadership actually looks like in banking, which roles and skills matter most, and how financial institutions can recruit for this function effectively.

Key Takeaways

- AI deployment in banking is outpacing governance — and the leadership needed to close that gap

- Responsible AI requires fairness, explainability, human oversight, data privacy, and continuous auditability

- Key roles: Chief AI Officer, AI Ethics Lead, Model Risk Manager, AI Compliance Officer, and Data Governance Lead

- Strong candidates typically come from model risk, regulatory affairs, fair lending, or legal backgrounds

- Filling these roles requires search expertise across compliance, risk, and technology — generalist recruiting falls short

Why Banks Are Under Pressure to Build Responsible AI Leadership

Regulatory pressure on AI-driven decisions in banking is no longer theoretical.

CFPB Circular 2023-03 made clear that when creditors use AI or complex models, generic adverse-action checklist reasons are not sufficient. The bank's duty to explain a credit denial to the consumer doesn't disappear because the model is complex — it requires specific, accurate reasons tied to the model's actual outputs.

The EU AI Act classifies AI systems that evaluate individual creditworthiness or establish credit scores as high-risk, triggering obligations around risk management, documentation, human oversight, and auditability. U.S. institutions with EU exposure need governance capabilities that can meet those standards.

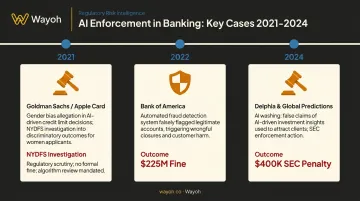

Enforcement examples make the stakes concrete:

| Institution | Year | Issue | Outcome |

|---|---|---|---|

| Bank of America | 2022 | Faulty automated fraud-detection froze unemployment benefit accounts | $225M fine from CFPB and OCC |

| Goldman Sachs / Apple Card | 2021 | Allegations of gender bias in credit underwriting | NYDFS investigation; no violation found, but transparency and customer-service deficiencies identified |

| Delphia & Global Predictions | 2024 | False claims about AI use in investment strategies | SEC charged both for "AI washing"; combined penalties of $400K |

These cases share a common thread: the absence of accountable, AI-literate leadership at the point where model decisions meet regulatory obligation. Financial institutions responding well to that pressure are building dedicated internal leadership functions for responsible AI, rather than delegating it to the CTO office or assuming general counsel will absorb it. That structural shift is creating a scarce and fast-growing category of talent demand.

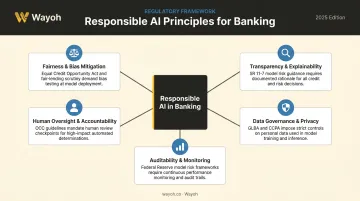

The Core Principles Responsible AI Leaders Must Champion

Understanding what "responsible AI" means in practice is essential before hiring for it. These aren't abstract values — they're operational requirements with regulatory teeth.

Fairness and Bias Mitigation

AI models trained on historical financial data can embed existing disparities in credit access, lending decisions, and customer treatment. Responsible AI leaders must understand bias detection methodologies and mandate debiasing across model development and deployment, not just audit for it after deployment.

Transparency and Explainability

The "black box" problem is a legal problem in banking. BIS FSI guidance on AI explainability distinguishes between explainability (can the output be explained to a human?) and interpretability (can the model's inner workings be understood?). Both matter differently across use cases.

In credit underwriting and fraud scoring, leaders must operationalize explainable AI approaches that satisfy consumers, examiners, and courts.

Human Oversight and Accountability

AI should augment human judgment in sensitive financial decisions, not replace it outright. Responsible AI leaders must establish clear protocols for:

- When human review is required before an AI-driven decision is final

- Who is accountable when an AI-driven decision causes consumer harm

- How escalation paths work when models produce unexpected outputs

Data Governance and Privacy

Responsible AI starts with governed, high-quality data. Leaders must own data quality from the top down, ensuring training data meets standards across:

- Accuracy and completeness before model ingestion

- Consent and compliance with GDPR, CCPA, and sector-specific rules

- Consistent enforcement across business lines, not just IT

Data governance at this level requires leadership-level accountability, not a delegated IT checklist.

Auditability and Ongoing Monitoring

AI models in banking are not set-and-forget deployments. The Federal Reserve, OCC, and FDIC issued revised model risk management guidance in April 2026 (SR 26-2 and OCC Bulletin 2026-13), updating the foundational SR 11-7 framework to address machine learning and generative AI.

Leaders must establish continuous monitoring for model drift, performance degradation, and unexpected outputs. Models must also withstand both internal review and regulatory audit — and that capability needs to be built in from day one.

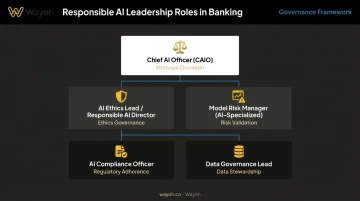

The Roles That Make Up a Responsible AI Leadership Team

The IIF-EY survey found that AI/ML governance most commonly sits with the Chief Risk Office or Chief Data Office (each at 27%), while only 8% of firms had a dedicated C-suite manager solely for AI/ML. That fragmentation reflects how early most institutions are. Here's what a more deliberate structure looks like:

Chief AI Officer (CAIO) or Head of AI

The executive-level owner of overall AI strategy — including how responsible AI principles are embedded across the institution. Unlike a CTO or CDO, the CAIO sits at the intersection of AI ambition and ethical governance, typically reporting to the CEO or board. Not every bank will create this title; many assign the function to a Chief Data or Chief Risk Officer.

AI Ethics Lead or Responsible AI Director

This function embeds fairness, transparency, and accountability into AI development workflows, operating cross-functionally with product, data science, legal, and compliance. Larger institutions with active model pipelines are increasingly hiring this as a standalone role, separate from the CAIO.

Model Risk Manager (AI-Specialized)

Model risk management is well-established in banking under SR 11-7. Machine learning and generative AI, however, introduce risks that traditional validators weren't trained for:

- Distributional shift as real-world data diverges from training sets

- Adversarial inputs that exploit model vulnerabilities

- Hallucinations and fabricated outputs in generative contexts

Candidates need AI-specific model risk expertise — not just standard validation credentials.

AI Compliance Officer

Some institutions are creating compliance roles focused specifically on AI regulatory obligations: mapping AI deployments to applicable laws, preparing for examiner inquiries, and managing disclosure requirements. The position sits at the intersection of legal, compliance, and technology.

Data Governance Lead (AI-Focused)

Many responsible AI failures originate in data — poor lineage, biased training sets, inadequate privacy controls. A data governance leader who understands AI's data dependencies is foundational to any responsible AI program at scale. Wayoh has direct placement experience here, supporting data governance hiring across fintech and banking clients.

Smaller institutions often consolidate several of these functions into one hire — particularly the compliance, ethics, and governance dimensions.

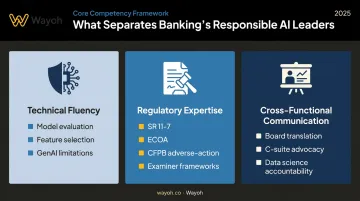

The Skill Set That Defines a Capable Responsible AI Leader

Technical Fluency — Not Engineering Depth

Responsible AI leaders don't need to build models. They do need to understand how machine learning models work: training data, feature selection, model evaluation, and the specific limitations of generative AI. Without this baseline, they can't meaningfully challenge technical teams, interpret risk assessments, or recognize when a validation report is incomplete.

Engineers own technical depth. Responsible AI leaders need technical fluency — enough to ask the right questions, push back on incomplete answers, and follow the logic without building the model themselves.

Financial Services Regulatory Expertise

This is the differentiator that separates responsible AI leaders in banking from their counterparts in other industries. Candidates must understand:

- Model risk management guidance (SR 11-7 and the 2026 revised guidance)

- Fair lending laws — ECOA, the Fair Housing Act, and their interaction with algorithmic decision-making

- Consumer protection frameworks, including the CFPB's adverse-action requirements

- How examiners from the OCC, FDIC, and Federal Reserve approach AI governance in examinations

Job postings from institutions like Citi and JPMorgan emphasize AI governance, model risk, data governance, compliance, and financial services regulatory experience more consistently than any specific certification. Background areas that translate well include compliance leadership, regulatory affairs, model validation, and JD-qualified candidates with financial services focus.

Cross-Functional Communication and Stakeholder Influence

Responsible AI governance fails in silos. The most effective leaders can:

- Translate AI risk for board members and regulators who aren't technical

- Advocate for governance investments with a C-suite that wants to move fast

- Hold data science teams accountable to ethical standards without being the expert in the room

The WEF Future of Jobs Report 2025 found 63% of employers identify skill gaps as the primary barrier to transformation — and in financial services, the gap between AI ambition and governance capability is particularly acute. This "bridge builder" profile is rare enough that institutions consistently struggle to fill these roles from internal pipelines — which is why compensation for qualified candidates has risen well above comparable compliance and risk leadership positions.

How to Recruit Responsible AI Leaders

Define the Role Before You Source

Many institutions treat responsible AI leadership as an extension of either technology or compliance. The job description must clearly articulate:

- Whether the role carries decision-making authority or is advisory

- Where it sits in the reporting structure (CTO, CRO, CEO, board?)

- What cross-functional authority it has — can this person pause an AI deployment?

Candidates evaluate these factors heavily. A governance role with no real power to stop a problematic model deployment will not attract the strongest candidates.

Look Beyond the Obvious AI Talent Pools

The conventional approach — recruiting from AI companies or data science teams — typically misses the regulatory dimension. Responsible AI leaders in banking often come from:

- Model risk management teams at major banks or the Federal Reserve

- Regulatory affairs and fair lending compliance functions

- Legal backgrounds with financial services and consumer protection focus

- Data governance leadership roles with AI exposure

Broadening search criteria to these populations — while screening for baseline AI fluency — is more likely to surface candidates who can actually operate in a regulated environment.

Assess for Principle and Pragmatism

Responsible AI leadership in banking is not a philosophy exercise. Strong candidates should demonstrate they can move programs forward within a risk-averse institution, not just articulate principles. In interviews, ask:

- Describe a governance framework you built from scratch — what did it include?

- Walk me through a situation where AI deployment timelines conflicted with governance requirements. What did you do?

- How would you explain model risk in a credit underwriting context to a board member with no technical background?

Candidates who answer in abstractions — without referencing specific controls, escalation paths, or institutional trade-offs — are unlikely to build credibility with risk committees or regulators.

Compete on Mission and Authority

Professionals drawn to responsible AI work tend to be motivated by impact — the opportunity to build something that matters, not just another compliance program. Banks and fintechs can attract strong candidates by communicating:

- The seniority and genuine authority of the role

- The institution's real commitment to governance (not just marketing language)

- That the role can actually influence AI deployment decisions, not just document them after the fact

Candidates will ask directly whether this role has real power. The honest answer to that question will do more for hiring success than any compensation package.

Partner with Specialized Recruiters

Finding candidates who combine AI governance knowledge with financial services regulatory expertise requires a recruiter who operates in both worlds. Generalist tech recruiters rarely screen for regulatory judgment or control experience. Compliance-only recruiters, on the other hand, often lack the AI fluency to assess whether a candidate can actually evaluate a model's risk architecture.

Wayoh focuses on compliance, risk, legal, and data governance hiring across major U.S. banking markets (including New York, California, and Florida), applying a human-first recruiting approach to every search. With 500+ placements across banking and fintech — including direct experience placing data governance and compliance leaders — Wayoh brings the regulated-industry context these searches require.

Frequently Asked Questions

What are the principles of responsible AI in banking?

The core principles are fairness and bias mitigation, transparency and explainability, human oversight, data governance, and auditability. Implementing these requires dedicated leadership and governance structures, not just policy statements — regulators and consumers expect both.

What kind of AI is used in banking?

Common applications include fraud detection, credit underwriting, AML monitoring, customer service automation, and generative AI for contract analysis. Each carries distinct responsible AI obligations under fair lending, consumer protection, and model risk management frameworks.

What roles make up a responsible AI leadership team in a bank?

Core roles include Chief AI Officer, AI Ethics Director, AI-specialized Model Risk Manager, AI Compliance Officer, and Data Governance Lead. Smaller institutions often consolidate these into a single hire, typically combining compliance, ethics, and governance responsibilities.

What is the difference between a Chief AI Officer and a Chief Technology Officer in banking?

A CTO oversees technology infrastructure and engineering broadly. A CAIO specifically owns AI strategy including governance, ethics, and responsible deployment, a distinction that matters as AI-driven decisions face increasing scrutiny from regulators and consumers.

How do you evaluate a candidate's responsible AI credentials during a banking interview?

Ask for concrete outcomes: governance frameworks they built, how they navigated conflict between deployment speed and compliance requirements, and whether they can explain AI risk to a non-technical regulator or board member. Abstract answers about principles aren't sufficient.

Why is it so hard to hire responsible AI leaders in financial services?

The role demands a rare combination of technical AI fluency, financial services regulatory expertise, and cross-functional leadership that doesn't map onto traditional career tracks. The candidate pool is genuinely small, and competition among institutions that have recognized the need is already intense.