That talent gap is specific. Banks don't need more data scientists, and they don't need traditional risk managers who've never touched an ML model. They need professionals who can do both — fluent in NIST AI RMF, grounded in SR 11-7 and its successor guidance, and capable of working across compliance, legal, and data science without losing credibility with any of them.

This article breaks down what that talent looks like, which roles matter most, what to assess during hiring, and how to find candidates who don't often show up on standard job boards.

Key Takeaways

- AI use in financial services is expanding into credit, fraud, AML, and risk functions — and regulators are watching closely

- The NIST AI RMF's four functions (Govern, Map, Measure, Manage) define what an AI risk team must actually do

- Five roles anchor a modern banking AI risk team: AI Risk Officer, Model Risk Validator, AI Governance Analyst, AI Ethics Specialist, and Compliance Lead

- Strong candidates bring quantitative or compliance backgrounds with direct regulatory and model risk experience, not just technical credentials

- Standard job boards rarely surface this talent — most placements require targeted outreach through specialist networks

Why Banks Are Urgently Hiring AI Risk Management Professionals

AI isn't experimental in banking anymore. BIS data suggests roughly 70% of financial firms now use AI to enhance cash-flow predictions, fraud detection, and credit scoring.

The 2021 interagency RFI from the Fed, OCC, FDIC, CFPB, and NCUA documented AI applications across fraud detection, BSA/AML investigations, credit decisions, underwriting, compliance monitoring, and internal audit.

Regulatory pressure is matching that expansion. The CFPB's 2022 guidance made clear that ECOA adverse-action requirements apply even when a complex algorithm makes the credit decision — there's no "black box" exemption. OCC enforcement actions against TD Bank and Bank of America in 2024 cited BSA/AML transaction monitoring weaknesses, rules and threshold failures, data input gaps, and model validation deficiencies. These aren't abstract risks.

The Talent Supply Problem

The structural challenge isn't a shortage of AI professionals or a shortage of risk professionals. It's that these two talent pools barely overlap:

- Traditional risk managers understand SR 11-7, model validation, and regulatory exams — but most have limited exposure to gradient boosting, LLMs, or adversarial testing

- Data scientists can build and tune models — but typically lack fair lending knowledge, validation independence experience, or the ability to write examination-ready documentation

- Regulatory examiners and consultants understand governance frameworks — but often haven't worked inside a live ML development environment

Banks have three options: hire from the narrow intersection of these pools, build hybrid talent through internal development, or do both. Banks have three options: hire from the narrow intersection of these pools, build hybrid talent through internal development, or pursue both simultaneously. GARP's 2024 survey found that more than 50% of firms use training programs to upskill for GenAI, while roughly one-third cite outright lack of skilled professionals. Most institutions end up running both tracks at once — all while competing for the same small candidate pool.

Understanding What AI Risk Frameworks Demand of Banking Teams

The NIST AI RMF in a Banking Context

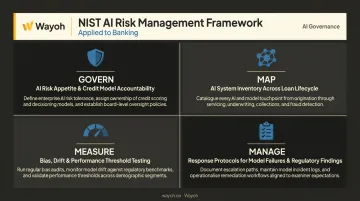

The NIST AI Risk Management Framework organizes AI risk management around four core functions:

| NIST Function | What It Means in Banking |

|---|---|

| Govern | Define AI risk appetite; assign accountability for AI-driven credit scoring models |

| Map | Inventory all AI systems and their data dependencies across the loan lifecycle |

| Measure | Test models for bias, drift, and performance against defined thresholds |

| Manage | Document responses to model failures, regulatory findings, and deployment decisions |

SR 11-7 and its anticipated successor guidance preserve core expectations around model inventory, materiality assessment, validation independence, monitoring, and governance documentation. Regulators treat these as the examination baseline — not aspirational standards.

EU AI Act Implications for Global Banks

Under the EU AI Act, AI systems used to evaluate the creditworthiness of natural persons or establish credit scores are classified as high-risk systems. That classification triggers mandatory requirements before deployment:

- Risk management systems

- Data governance controls

- Technical documentation

- Logging and audit trails

- Human oversight mechanisms

- Conformity assessment

For banks operating across jurisdictions, this adds a compliance layer that U.S. frameworks don't fully address. Professionals with working knowledge of both U.S. regulatory guidance and the EU AI Act's high-risk obligations are rare — and demand for them is growing.

That cross-jurisdictional gap shapes what banking teams actually need when they hire. Every AI risk role maps to one or more of these four risk categories.

Four AI Risk Types That Shape Hiring

Every role on a banking AI risk team maps to one or more of these risk categories:

- Data risks — biased training data, data poisoning, privacy breaches, data lineage failures → requires data governance and validation experience

- Model risks — adversarial attacks, model drift, interpretability failures, conceptual unsoundness → requires ML validation and explainability skills

- Operational risks — integration failures, lack of accountability structures, third-party model dependency → requires operational resilience and vendor risk experience

- Ethical/legal risks — algorithmic bias in lending, ECOA adverse-action failures, GDPR and Fair Lending non-compliance → requires fair lending, UDAAP, and CRA knowledge

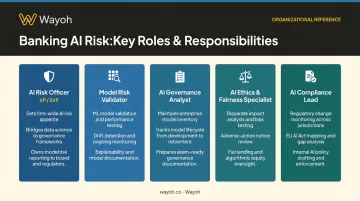

Key Roles That Make Up a Modern Banking AI Risk Team

A complete AI risk function in banking isn't a single hire — it's a set of distinct, interdependent roles. Each one covers a different slice of the risk surface, from model validation to regulatory readiness. Here's how these roles break down in practice.

AI Risk Officer / Head of AI Risk

This is the senior accountability role. The AI Risk Officer sets the organization's AI risk appetite, oversees framework implementation, and serves as the bridge between data science and risk governance committees. At most larger institutions, this sits at VP to SVP level.

What makes it hard to fill: the role requires both executive communication skills and genuine technical grounding. A candidate who can write a board memo but can't assess a gradient boosting model's validation methodology won't hold credibility with the data science teams they're supposed to govern.

Model Risk Validator / SR 11-7 Specialist

Independent model validation has always been a core regulatory requirement. What's changed is the subject matter. As banks replace logistic regression with ensemble models and neural networks in credit and fraud, validators need to assess:

- Conceptual soundness of ML architectures

- Data lineage and feature engineering risks

- Explainability approaches such as SHAP and LIME

- Ongoing monitoring and drift detection protocols

Candidates who only know how to validate traditional statistical models are increasingly mismatched for what the actual model inventory contains.

AI Governance Analyst

A mid-level role that bridges compliance and technology. Primary responsibilities include:

- Maintaining AI model inventories (also called an AI Bill of Materials, or AI-BOM)

- Tracking the AI lifecycle from development through decommission

- Ensuring documentation meets regulatory expectations during exams

This role often comes from a compliance operations or regulatory reporting background, with enough technical exposure to communicate with model developers.

AI Ethics and Fairness Specialist

Following CFPB Circular 2022-03 — which confirmed that ECOA adverse-action requirements apply to complex algorithmic credit decisions — fair lending compliance for AI systems is a named regulatory priority. This role handles:

- Disparate impact analysis on lending and underwriting models

- Bias testing across protected class attributes

- Ensuring adverse-action notices are model-specific and legally defensible

Candidates typically come from fair lending compliance, consumer protection law, or quantitative analysis backgrounds — prior exposure to credit model documentation is a strong differentiator.

AI Compliance Lead / Regulatory Affairs Specialist

Tracks the regulatory horizon and translates it into internal policy. Core responsibilities include:

- Monitoring CFPB guidance, OCC bulletins, and state-level AI legislation

- Mapping EU AI Act implementation timelines for global institutions

- Building internal policy ahead of examiner scrutiny, not in response to it

Skills and Qualifications to Look for When Hiring AI Risk Talent

Technical Skills Worth Assessing

Candidates don't need to be data scientists — but they need enough technical fluency to hold their own with the teams they oversee. Assess for:

- Familiarity with common ML model types: gradient boosting, neural networks, LLMs

- Understanding of model validation methodology: conceptual soundness, outcomes analysis, benchmarking

- Working knowledge of explainability methods, particularly SHAP (which FinRegLab research notes is increasingly favored over LIME for credit applications)

- Data pipeline governance, feature engineering awareness, and data quality controls

Regulatory and Compliance Knowledge

This is where many technically strong candidates fall short. The regulatory baseline for banking AI risk includes:

- SR 11-7 / SR 26-2 model risk management guidance and what's changed between them

- OCC's guidance on third-party AI risk and model inventory expectations

- CFPB's algorithmic adverse-action requirements under Regulation B

- BSA/AML model risk: threshold-setting, alert logic, customer risk rating validation

- Awareness of NIST AI RMF as an operating framework

Certifications provide a useful signal, though none cover the full scope of this role on their own.

Certifications worth evaluating: GARP's FRM and its Risk & AI (RAI) credential signal financial risk foundations. CAMS is relevant for candidates targeting BSA/AML model risk roles. No official NIST AI RMF practitioner credential exists yet — ask for demonstrated working knowledge instead.

Cross-Functional Communication

Strong candidates need to work effectively in both directions. Look for the ability to:

- Translate AI risk findings into board-level reporting and examination-ready documentation

- Maintain credibility with technical teams, legal counsel, and senior leadership

- Communicate model decisions clearly to non-technical examiners under scrutiny

Candidates who excel in one direction but not both typically create gaps that surface during regulatory reviews.

Red Flags to Screen For

- Pure technical background with no regulatory or governance exposure

- Cannot explain model decisions in plain language to a non-technical examiner

- No experience with validation independence requirements

- Unfamiliar with how examiners assess model risk during safety and soundness reviews

- Treats "AI ethics" as a philosophical concept rather than a compliance and documentation discipline

How to Source and Attract Qualified AI Risk Professionals

Where This Talent Actually Lives

The candidate pool with genuine AI/ML fluency and banking regulatory knowledge is small — and actively targeted by the largest banks, Big Four consulting firms, and occasionally regulators themselves. A few realities:

- Standard job boards surface the active, often less specialized portion of this market

- Most strong candidates in this space are passive — they're employed, performing well, and not refreshing LinkedIn job alerts

- Referral networks and specialist recruiting relationships surface the candidates that job postings don't

GARP's 2024 Risk Careers Survey found 73% of risk professionals expect opportunities to increase over the next 18 months and 54% expect risk-team staffing to rise — with AI risk among the leading hiring areas. That demand pressure is already squeezing supply.

What Makes These Roles Attractive to Candidates

Banks that compete successfully for this talent tend to offer more than salary. Strong value propositions include:

- Actual governance authority with accountability, not purely advisory functions

- Exposure to complex, high-stakes AI implementations that rarely exist outside of banking

- Direct engagement with regulators on novel, unresolved AI questions — a genuine draw for this profile

- Compensation benchmarked across both risk and technology pay scales, not just one or the other

The BLS reports a May 2024 median annual wage of $106,000 for financial risk specialists — a reasonable floor reference, though senior AI risk roles at larger institutions commonly range from $150,000–$200,000+, depending on scope and location.

The Case for Specialist Recruiting Support

For most banks, building a sourcing capability for AI risk talent from scratch isn't practical. The search requires simultaneous engagement across compliance, model validation, data governance, and AI governance networks — most of which operate through relationships, not job postings.

Wayoh works this market through its existing network of 500+ placed professionals across compliance, risk, and legal functions in banking and fintech. Grounded in a human-first recruiting philosophy, that network includes model risk validators, compliance leaders, data governance specialists, and financial crime professionals who are increasingly working at the intersection of regulation and AI. Searches start with direct conversations with known professionals — many of whom aren't actively looking but are assessable through prior relationships.

Frequently Asked Questions

What is the AI risk management framework?

An AI risk management framework is a structured set of practices for identifying, assessing, and mitigating AI-related risks across the full AI lifecycle. The NIST AI RMF is the most widely adopted standard, organized around four core functions: Govern, Map, Measure, and Manage.

What are the four types of AI risk?

The four main categories are:

- Data risks: bias, breaches, data integrity failures

- Model risks: adversarial attacks, drift, interpretability failures

- Operational risks: integration failures, lack of oversight, third-party dependency

- Ethical/legal risks: algorithmic bias, adverse-action non-compliance, fair lending violations

What are the five pillars of an AI framework?

No single regulator defines a "five pillars" standard for banking AI. A practical model drawn from NIST, OCC/Fed guidance, and FSB/BIS risk taxonomies maps to five areas:

- Governance and accountability

- Data and model lifecycle controls

- Validation and measurement

- Human oversight and compliance

- Monitoring, incident response, and third-party oversight

What qualifications should an AI risk manager in banking have?

Strong candidates combine a quantitative or compliance background with direct model risk or AI governance experience, working knowledge of SR 11-7/SR 26-2, and the ability to bridge technical and regulatory functions. Credentials like FRM, CAMS, or GARP's RAI designation support the profile but don't substitute for hands-on validation experience.

How is AI risk in banking different from AI risk in other industries?

Banking AI risk carries heightened stakes due to direct regulatory oversight (OCC, Fed, CFPB), fair lending laws that apply to algorithmic decisions, and the systemic risk of model failures in credit, fraud, and AML. The hiring bar is higher as a result — regulatory exam readiness and compliance accountability are non-negotiable.

What is the difference between an AI risk manager and a traditional model risk manager?

Traditional model risk managers focused on statistical and quantitative models under SR 11-7. AI risk managers must also address black-box explainability, adversarial ML risks, and LLM-specific vulnerabilities. Their scope extends beyond validation into deployment monitoring, ethics documentation, and cross-jurisdictional regulatory compliance.